Using T-Accounts to Analyze Transactions PowerPoint PPT Presentation

1 / 18

Title: Using T-Accounts to Analyze Transactions

1

Using T-Accounts to Analyze Transactions

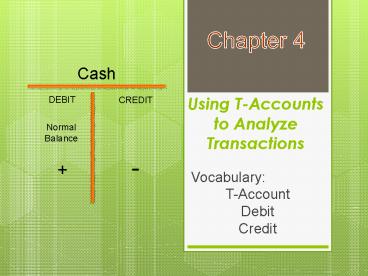

Chapter 4

Cash

DEBIT

CREDIT

Normal Balance

-

Vocabulary T-Account Debit Credit

2

What you already (should) know!

Chapter 4

- Basic Accounting Equation

- Assets Liabilities Owners Equity

- Assets

- Anything of value owned by a business.

- Cash, Supplies, Prepaid Insurance

- Liability

- Anything owed by a business

- Accounts Payable (Tractor Supply Company)

- Owners Equity

- The rights the owner has to the things owned by

the business. - Capitalinvestment from the owner

- Drawingpaid to the owner for personal use

- Revenue

- Money received from the operation of the business

- Sales, Fees

- Expenses

- Money paid out from the operation of the

business. - Rent Expense, Uttilities Expense,

3

What you are going to learn

Chapter 4

- T-Accounts

- A simple tool used to aid in the analysis of

business transactions. - Represents the left and right side of an account

- DebitLeft side of an account

- CreditRight side of an account

- Every transaction

- Changes at least 2 accounts

- Involves 1 Debit entry and 1 Credit entry

- Account Balances

- Are increased on the same side as an accounts

normal balance - Are decreased on the opposite side of an

accounts normal balance

4

Chapter 4

Account Title

Debit Left Side of an Account

Credit Right Side of an Account

5

Normal balance of Accounts are determined by

their placement on the basic Accounting Equation

Chapter 4

Debit

Credit

ASSETS Accounts have DEBIT balances

LIABILITIES And OWNERS EQUITY Accounts have

CREDIT balances

6

Going back to our new rule--Increase on SAME

side as normal balance --Decrease on OPPOSITE

side of normal balance

Chapter 4

- Asset

- Increases on the debit (left) side

- Decreases on the credit (right) side

- Liability

- Increases on the credit (right) side

- Decreases on the debit (left) side

- Capital

- Increases on the credit (right) side

- Decreases on the debit (left) side

7

Normal balances of Revenue, Expenses and Drawing

are determined by their relationship to the

Capital account.

Chapter 4

John Smith, Captial

Debit

Credit

Normal Balance

Debit to decrease Capital

Credit to increase Capital

Expenses and Drawing have Debit balances because

they decrease Capital

Revenue has a Credit balance because it increases

Capital

8

How Do We Determine If An Account Is Debited or

Credited?

Chapter 4

- Memorization at first

- Determine an accounts balance side

- Increase on balance side

- Decrease on opposite side

- It will eventually become intuitive

9

Remember for every transaction

Chapter 4

- Every business transaction must have at least one

debit and one credit.

10

Samples

Chapter 4

Analyze transactions into Debit and Credit parts.

11

Received Cash from the owner as an investment

1,000.

Chapter 4

Cash

Capital

Debit

Credit

Debit

Credit

NB

NB

1,000

1,000

12

Paid Cash for Supplies 500.

Chapter 4

Cash

Supplies

Debit

Credit

Debit

Credit

NB

NB

-

500

500

13

Paid Cash for Insurance 1,200.

Chapter 4

Cash

Prepaid Insurance

Debit

Credit

Debit

Credit

NB

NB

-

1,200

1,200

14

Bought Supplies on account from Smith Company, AP

800.

Chapter 4

Supplies

Smith Co.,AP

Debit

Credit

Debit

Credit

NB

NB

800

800

15

Paid Cash on account to Smith Company, AP 500.

Chapter 4

Cash

Smith Co.,AP

Debit

Credit

Debit

Credit

NB

NB

-

-

500

500

16

Received Cash from Sales 2,000.

Chapter 4

Cash

Sales

Debit

Credit

Debit

Credit

NB

NB

2,000

2,000

17

Paid Cash for the Electric Bill 200.

Chapter 4

Cash

Utilities Expense

Debit

Credit

Debit

Credit

NB

NB

-

200

200

18

Paid Cash to the owner for Personal Use 500.

Chapter 4

Cash

Drawing

Debit

Credit

Debit

Credit

NB

NB

-

500

500

Recommended