The Accounting Cycle PowerPoint PPT Presentation

1 / 78

Title: The Accounting Cycle

1

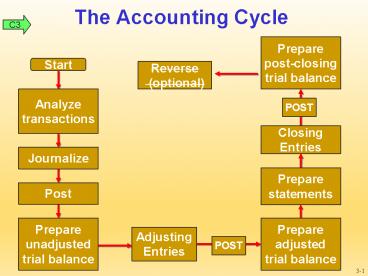

The Accounting Cycle

C3

Preparepost-closingtrial balance

Start

Reverse (optional)

Analyzetransactions

POST

Closing Entries

Journalize

Preparestatements

Post

Prepareunadjustedtrial balance

Prepareadjustedtrial balance

Adjusting Entries

POST

3-1

2

The Accounting Processing Cycle

3

The Account and its Analysis

C 3

2-3

4

The Accounting Equation

A L OE

5

Accounting Equation for a Corporation

A L SE

6

The Account and its Analysis

C 3

Liabilities

Equity

Assets

2-6

7

Asset Accounts

C 3

Cash

Accounts Receivable

Land

AssetAccounts

Notes Receivable

Buildings

Prepaid Accounts

Equipment

Supplies

2-7

8

Liability Accounts

C 3

Notes Payable

Accounts Payable

LiabilityAccounts

Dividends Payable

Accrued Liabilities

Unearned Revenue

2-8

9

Equity Accounts

C 3

Retained Earnings

CommonStock

Dividends Declared

EquityAccounts

Revenues

Expenses

2-9

10

The Account and its Analysis

C 3

An account is a record of increases and decreases

in a specific asset, liability, equity, revenue,

or expense item.

The general ledger is a record containing all

accounts used by the company.

2-10

11

Ledger and Chart of Accounts

C 4

The ledger is a collection of all accounts for

aninformation system. A companys size and

diversity of operations affect the number of

accounts needed.

The chart of accounts is a list of all accounts

andincludes an identifying number for each

account.

2-11

12

Debits and Credits

C 5

- A T-account represents a ledger account and

is a tool used to understand the effects of one

or more transactions.

2-12

13

General Ledger

The T account is a shorthand format of an

account used by accountants to analyze

transactions.

14

Double-Entry AccountingNORMAL Balance

ASSETS LIABILITIES EQUITY DR

CR CR Assets are

on the left side of the equation therefore, the

left, or debit side is the normal balance side

for assets. Liabilities and equities are on the

right side therefore, the right, or credit side

is the normal balance side for liabilities and

equity.

15

Double-Entry Accounting

ASSETS LIABILITIES EQUITY

ASSETS LIABILITIES Common Stock DIV

REV EXP DR CR CR DR CR

DR

Total amount that is debited to accounts must

equal the total amount credited to accounts for

each transaction. Sum of debit account balances

in the ledger must equal the sum of credit

account balances.

16

Double-Entry AccountingNORMAL Balance

C 5

Whether a debit or a credit is an increase or

decrease depends on the NORMAL Balance of the

account.

2-16

17

Double-Entry AccountingNORMAL Balance

C 5

Equity

2-17

18

Double-Entry AccountingNORMAL Balance

C 5

- An account balance is the difference

between the increases and decreases in an

account. - Notice the T-Account

2-18

19

Journalizing Posting Transactions

P1

2-19

20

Journalizing Transactions

P1

- Dollar amount of debits and credits

2-20

21

Balance Column Account

P1

- T-accounts are useful illustrations, but

balance column accounts are used in practice.

2-21

22

Posting Journal Entries

P1

1

Identify the debit account in ledger.

2-22

23

Posting Journal Entries

P1

2

Enter the date.

2-23

24

Posting Journal Entries

P1

3

Enter the amount and description.

2-24

25

Posting Journal Entries

P1

Enter the journal reference.

4

2-25

26

Posting Journal Entries

P1

Compute the balance.

5

2-26

27

Posting Journal Entries

P1

Enter the ledger reference.

6

2-27

28

Analyzing Transactions

A1

2-28

29

Analyzing Transactions

A1

2-29

30

Analyzing Transactions

A1

Analysis

2-30

31

Analyzing Transactions

A1

Analysis

2-31

32

Analyzing Transactions

A1

2-32

33

Analyzing Transactions

A1

2-33

34

After processing its remaining transactions for

December, FastForwards Trial Balance is prepared.

A1

2-34

35

The Accounting Cycle

C3

Preparepost-closingtrial balance

Start

Reverse (optional)

Analyzetransactions

POST

Closing Entries

Journalize

Preparestatements

Post

Prepareunadjustedtrial balance

Prepareadjustedtrial balance

Adjusting Entries

POST

3-35

36

The Adjustment Process

Accounts are adjusted at the end of a period to

record internal transactions and events that are

not yet recorded. Two basic principles for

recognizing Revenues and Expenses 1. The

revenue recognition principle requires revenue be

recorded when earned, not before and not

after. 2. The matching principle requires

expenses be recorded in the same period as the

revenues earned as a result of these expenses.

37

Accrual Basis versus Cash Basis

Accrual basis accounting uses the adjusting

process to recognize revenue when earned and to

match expenses with revenues. This means the

economic effects of revenues and expenses are

recorded when earned or incurred, not when cash

is received or paid. Accrual basis is consistent

with GAAP. Cash basis accounting revenues are

recognized when cash is received and expenses are

recognized when cash paid. Cash basis is not

consistent with GAAP. Accrual accounting also

increases the comparability of financial

statements from one period to another.

38

Accrual Basis vs. Cash Basis

C 1

Cash Basis Revenues are recognized when cash is

received and expenses recorded when cash is paid.

Accrual Basis Revenues are recognized when earned

and expenses are recognized when incurred.

Accounting

3-38

39

Accrual Basis vs. Cash Basis

C 1

On the cash basis the entire 2,400 would be

recognized as insurance expense in 2009. No

insurance expense from this policy would be

recognized in 2010 or 2011, periods covered by

the policy.

3-39

40

Accrual Basis vs. Cash Basis

C 2

On the accrual basis, Insurance expense is

recognized as follows100 in 2009, 1,200 in

2010, and 1,100 in 2011. The expense is matched

with the periods benefited by the insurance

coverage.

3-40

41

Adjusting Accounts

An adjusting entry is recorded to bring an asset

or liability account balance to its proper

amount. The adjusting process is based on

ACCRUAL ACCOUNTING of Revenue Recognition and

Matching Principle. Adjusting accounts is a

3-step process (1) Determine the current

account balance, (2) Determine what the current

account balance should be, and (3) Record

adjusting entry to get from step 1 to step 2.

42

Adjusting Accounts

C2, P1

Framework for Adjustments

Adjustments

including depreciation

3-42

43

Supplies

Prepaid (Deferred) Expenses

P1

- During 2009, Scott Company purchased 15,500

of supplies. Scott recorded the expenditures as

Supplies. On December 31, a count of the supplies

indicated 2,655 on hand. - What adjustment is required?

3-43

44

Depreciation

P1

- Depreciation is the process of computing

expense from allocating the cost of plant and

equipment over their expected useful lives.

3-44

45

Depreciation

P1

- On January 1, 2009, Barton, Inc. purchased

equipment for 62,000 cash. The equipment has an

estimated useful life of 5 years and Barton

expects to sell the equipment at the end of its

life for 2,000 cash. - Lets record depreciation expense for the

year ended December 31, 2009.

3-45

46

Depreciation

P1

On January 1, 2009, Barton, Inc. purchased

equipment for 62,000 cash. The equipment has an

estimated useful life of 5 years and Barton

expects to sell the equipment at the end of its

life for 2,000 cash. Lets record

depreciation expense for the year ended December

31, 2009.

3-46

47

Depreciation

P1

Equipment is shown net of accumulated

depreciation. This amount is referred to as the

assets book value

3-47

48

Unearned (Deferred) Revenues

P1

Revenue

Credit Adjustment

Debit Adjustment

3-48

49

Unearned (Deferred) Revenues

P1

- On October 1, 2009, Ox University sold 1,000

season tickets to its 20 home basketball games

for 100 each. Ox University makes the following

entry

3-49

50

Unearned (Deferred) Revenues

P1

- On December 31, Ox University has played 10

of its regular home games, winning 2 and losing 8.

3-50

51

Accrued Expenses

P1

Were about one-half done with this job and want

to be paid forour work!

Costs incurred in a period that are both unpaid

and unrecorded.

3-51

52

Accrued Expenses

P1

Barton, Inc. pays its employees every Friday.

Year-end, 12/31/09, falls on a Wednesday. As of

12/31/09, the employees have earned salaries of

47,250 for Monday through Wednesday.

3-52

53

Accrued Expenses

P1

Barton, Inc. pays its employees every Friday.

Year-end, 12/31/09, falls on a Wednesday. As of

12/31/09, the employees have earned salaries of

47,250 for Monday through Wednesday.

3-53

54

Accrued Revenues

P1

Smith Jones, CPAs, had 31,200 of work

completed but not yet billed to clients. Lets

make the adjusting entry necessary on December

31, 2009, the end of the companys fiscal year.

3-54

55

3-55

56

The Accounting Cycle

C3

Preparepost-closingtrial balance

Start

Reverse (optional)

Analyzetransactions

POST

Closing Entries

Journalize

Preparestatements

Post

Prepareunadjustedtrial balance

Prepareadjustedtrial balance

Adjusting Entries

POST

3-56

57

- Prepare Income Statement

P3

3-57

58

- Prepare Statement of Retained Earnings

P3

Note Net Income from the Income Statement

carries to the Statement of Retained Earnings.

3-58

59

P3

- Prepare Balance Sheet

3-59

60

The Accounting Cycle

C3

Preparepost-closingtrial balance

Start

Reverse (optional)

Analyzetransactions

POST

Closing Entries

Journalize

Preparestatements

Post

Prepareunadjustedtrial balance

Prepareadjustedtrial balance

Adjusting Entries

POST

3-60

61

The Closing Process Temporary and Permanent

Accounts

C3

Temporary (nominal) accounts accumulate data

related to one accounting period. They include

all income statement accounts, the dividends

account, and the Income Summary account. These

accounts are closed at the end of the period to

get ready for the next accounting period.

Permanent (real) accounts report activities

related to one or more future accounting periods.

They carry ending balances to the next accounting

period and are not closed.

3-61

62

The Closing Process

63

Recording Closing Entries

P4

- Close revenue accounts to Inc. Summary

- Close expense accounts to Inc. Summary

- Close the income summary to RE

- Close dividends account to RE.

3-63

64

Recording Closing Entries

P4

Salaries Expenses

Consulting Revenues

25,000

18,100

Examine the accounts presented.

Retained Earnings

Income Summary

7,000

3-64

65

Recording Closing Entries

P4

Salaries Expenses

Consulting Revenues

Close revenues with a debit to the revenue

account and a credit to Income Summary.

25,000

18,100

Income Summary

Consulting Revenues 25,000 Income

Summary 25,000

3-65

66

Recording Closing Entries

P4

Salaries Expenses

Consulting Revenues

25,000

25,000

18,100

Close expense accounts with a credit to expenses

and a debit to Income Summary.

Income Summary

25,000

Income Summary 18,000 Salaries Expenses

18,000

3-66

67

Recording Closing Entries

P4

Salaries Expenses

Consulting Revenues

25,000

25,000

18,100

18,100

Income Summary

Determine the balance in the Income Summary

account.

18,100

25,000

3-67

68

Recording Closing Entries

P4

Income Summary 6,900 Retained Earnings

6,900

Salaries Expenses

18,100

18,100

Close the Income Summary to Retained Earnings.

Retained Earnings

Income Summary

18,100

25,000

7,000

6,900

3-68

69

Recording Closing Entries

P4

- The dividends account is closed to Retained

Earnings.

Retained Earnings

Dividends

2,000

7,000

6,900

3-69

70

Recording Closing Entries

P4

- The dividends account is closed to Retained

Earnings.

Dividends

Retained Earnings

2,000

2,000

2,000

7,000

6,900

11,900

Determine the ending balance in Retained Earnings.

3-70

71

Post Closing Trial Balance

P5

- Trial Balance prepared after the closing entries

have been posted. - The purpose is to insure that all nominal or

temporary accounts have been closed. - The only accounts on this trial balance should be

assets, liabilities, and equity accounts.

3-71

72

3-72

73

Let's prepare the Closing Entries for Dress

Right Corporation

74

(No Transcript)

75

.

CLOSING ENTRIES

Using the adjusted trial balance of 7/31, we can

prepare the following closing entries

1. To close the revenue accounts to income

summary

2. To close the expense accounts to income

summary

3. To close the income summary account to

retained earnings

76

CLOSING ENTRIES

Additional Consideration An alternative method

of recording a cash dividend is to debit a

temporary account called dividends, rather than

debiting retained earnings. If this approach is

used, an additional closing entry is required to

close the dividend account to retained earnings,

as follows

4. To close dividends to retained earnings

This is NOT the case with Dress Right

Corporation

77

Post-Closing Trial Balance

Lists permanent accounts and their balances.

Total debits equal total credits.

78

The Accounting Cycle

C3

Preparepost-closingtrial balance

Start

Reverse (optional)

Analyzetransactions

POST

Closing Entries

Journalize

Preparestatements

Post

Prepareunadjustedtrial balance

Prepareadjustedtrial balance

Adjusting Entries

POST

3-78

Recommended