GrahamHarvey 2001: TheoryPractice of Corporate Finance - PowerPoint PPT Presentation

Title:

GrahamHarvey 2001: TheoryPractice of Corporate Finance

Description:

Graham-Harvey (2001): Theory-Practice of Corporate Finance ... ratio, but instead use external financing only when internal funds are ... – PowerPoint PPT presentation

Number of Views:69

Avg rating:3.0/5.0

Title: GrahamHarvey 2001: TheoryPractice of Corporate Finance

1

Graham-Harvey (2001) Theory-Practice of

Corporate Finance

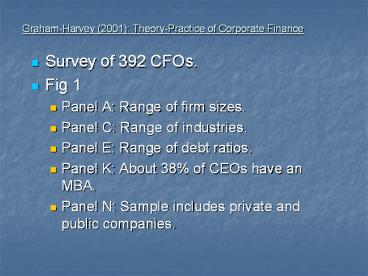

- Survey of 392 CFOs.

- Fig 1

- Panel A Range of firm sizes.

- Panel C Range of industries.

- Panel E Range of debt ratios.

- Panel K About 38 of CEOs have an MBA.

- Panel N Sample includes private and public

companies.

2

Graham-Harvey (2001) Theory-Practice of

Corporate Finance

- Fig 2 Popularity of different capital budgeting

techniques (in order) - IRR

- NPV

- Hurdle rate

- Payback

- Large firms, highly levered firms, and firms with

MBA-CEOs more likely to use NPV method.

3

NPV and IRR

Security Market Line (CAPM)

Accept

Expected Return

Reject

Rf

Beta

4

NPV and IRR

Expected Return

Accept

IRR

Cost of Capital

Reject

Beta

5

NPV and IRR

Security Market Line (CAPM)

A

Expected Return

B

Cost of Capital

C

D

Rf

Beta

A CAPM (Accept), CoC (Accept) B CAPM (Reject),

CoC (Accept) C CAPM (Accept), CoC (Reject) D

CAPM (Reject), CoC (Reject)

6

Graham-Harvey (2001) Theory-Practice of

Corporate Finance

- Fig 3 Popularity of different methods for

calculating cost of equity capital (in order) - CAPM

- Average historical return

- Multibeta CAPM

- Large firms, low levered firms, and firms with

MBA-CEOs more likely to use CAPM.

7

Graham-Harvey (2001) Theory-Practice of

Corporate Finance

- Fig 5 Factors that CFOs thought determined the

appropriate amount of debt (in order) - Financial flexibility (p. 218 minimizing

interest obligations such that they do not need

to shrink their business in case of an economic

downturn). - Credit rating.

- Earnings and cash flow volatility.

- Insufficient internal funds.

- Level of interest rates.

- Interest tax savings.

- Transaction cost and fees.

- Equity misvaluation.

- Comparable firm debt levels.

- Bankruptcy/distress costs.

8

Graham-Harvey (2001) Theory-Practice of

Corporate Finance

- Fig 7 Factors that CFOs thought relevant in

deciding whether or not to issue stock (in

order) - Earnings per share dilution.

- Stock misvaluation.

- Recent rise in stock price.

- Providing shares for employee/bonus stock option

plans. - Maintaining target debt-to-equity ratio.

- Diluting holding of certain shareholders.

- Stock is least risky source of funds.

9

Graham-Harvey (2001) Theory-Practice of

Corporate Finance

- 5.1. Tradeoff theory of capital structure choice

Firms have optimal debt-equity ratios which they

determine by trading off the benefits of debt

(tax advantage of interest deductibility), with

the costs of debt (financial distress costs, and

tax expense incurred by bondholders). - Fig 5 Corporate tax advantage of debt only

moderately important. - Fig 5 Financial distress moderately important.

But credit rating may be a proxy for financial

distress costs. - Fig 5 Personal tax considerations appears to be

not important.

10

Graham-Harvey (2001) Theory-Practice of

Corporate Finance

- 5.2. Asymmetric information explanations of

capital structure choice - 5.2.1 Pecking-order theory Firms do not target a

specific debt ratio, but instead use external

financing only when internal funds are

insufficient External funds are less desirable

because informational asymmetries between

management and investors imply that external

funds are undervalued. Hence, if firms use

external funds, they prefer to use debt,

convertible securities, and, as a last resort,

equity. - Table 9 Consistent with the pecking-order theory

Having insufficient internal funds is a

moderately important influence on the decision to

issue debt, especially for smaller firms (that

are likely to suffer from greater

asymmetric-information-related equity

undervaluation).

11

Graham-Harvey (2001) Theory-Practice of

Corporate Finance

- 5.2. Asymmetric information explanations of

capital structure choice - 5.2.2 Recent increase in stock price A surge in

share price increase can correct an

undervaluation or lead to an overvaluation. - Table 8 Recent stock price increase third most

important factor in equity-issuance decision. - 5.2.4 Convertible debt issuance Conversion

feature makes convertible debt relatively

insensitive to asymmetric information (between

management and investors) about the risk of the

firm. - Table 10 Firms use convertible debt to attract

investors unsure about the riskiness of the firm

(more relevant for smaller firms).

12

Graham-Harvey (2001) Theory-Practice of

Corporate Finance

- 5.3. Underinvestment problem

- Table 6 Consistent with theory underinvestment

more of a concern for growth firms compared to

non-growth firms. - Table 6 Overall, underinvestment does not appear

to be a major concern.

13

- What Do We Know About Capital Structure

- Rajan-Zingales (1995)

- Factors Correlated with Leverage

- 1. Tangibility of Assets

- Tangible assets can serve as collateral,

diminishing the risk of the lender. - Assets would retain more value in case of

liquidation.

14

- Factors Correlated with Leverage

- 2. Investment Opportunities

- The Underinvestment Problem With risky debt

outstanding, shareholders may sometimes not

undertake positive NPV projects. - Company Value Value of Tangible Assets in Place

Value of Future Growth Opportunities - V TA G

- V/TA 1 G/TA

- Market/Book Correlated with Growth

Opportunities. - Hence, high Market/Book companies (because they

have more future growth opportunities) will issue

less debt (be less levered).

15

- Factors Correlated with Leverage

- 2. Investment Opportunities

- High Market/Book companies (because they have

more future growth opportunities) will issue less

debt (be less levered). - Implying negative correlation between market/book

and leverage. - Rajan-Zingales (1995) Page 1456

- The negative correlation of market-to book with

leverage seems to be driven mainly by large

equity issuers. - Above evidence for companies in the US, Japan,

UK, and Canada. - From a theoretical standpoint, the evidence is

puzzling. If the market-to-book ratio proxies for

the underinvestment costs associated with high

leverage, then firms with high market-to-book

ratios should have low debt, independent of

whether they raise equity internally via retained

earnings, or externally. - Firms attempt to time the market by issuing

equity when their price (and hence, their

market-to-book ratio) is perceived to be high.

16

- Factors Correlated with Leverage

- 3. Size

- Larger firms tend to be more diversified and fail

less often, so size may be an inverse proxy for

the probability of bankruptcy. Hence, larger

firms may issue more debt. - 4. Profitability

- More profitable companies use less debt.

- Firms cash flow identity

New debt New equity Net income Interest

payment Dividend New investment

17

- Firms Histories and Their Capital Structures

- Kayhan-Titman (2004)

- Optimal Capital Structure Tradeoffs between the

costs and benefits of debt. - At the optimum Relation between capital

structure and firm value may be weak, such that

cost of deviating from the optimum is small. - When this is the case, capital structures are

likely to be strongly influenced by transaction

costs and market considerations that may

temporarily affect the relative costs of debt

versus equity financing, making the idea of a

target debt ratio much less important.

18

- Debt-Value Function

V0

Value of Company

V1

V2

D1

D0

D2

Debt/Total Capital

19

- Debt-Value Function

- Small deviations from optimal capital structure,

D0, may not have a big impact on firm value.

V0

Value of Company

D0

Debt/Total Capital

20

- Table A2 Predicting Leverage

- Leverage is positively related to

- Property, plant, and equipment

- Size.

- Leverage is negatively related to

- Market-to-book

- Profitability

- Selling expense

- RD.

- Leverage Deficit Actual Leverage Predicted

Leverage

21

- Table 3 Leverage

- Prior stock returns have a very significant

impact on capital structure. - Prior stock returns might also lead to a change

in target capital structure. - High stock returns might signal more growth

opportunities suggesting lower debt ratios. - As firm performs better, managers may get

entrenched. Managers prefer less debt (than

optimal) because they personally incur bankruptcy

costs and have less discretion in more levered

firms.

Recommended

CrystalGraphics Presentations