Utility Theory PowerPoint PPT Presentation

Title: Utility Theory

1

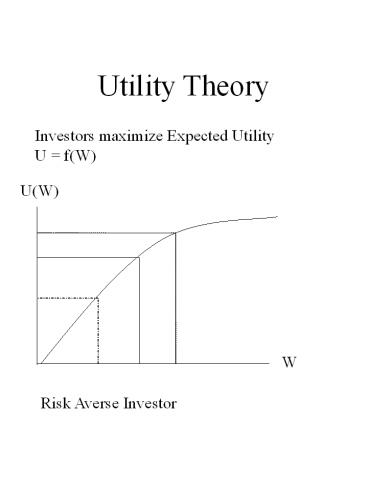

Utility Theory

Investors maximize Expected Utility U f(W)

U(W)

W

Risk Averse Investor

2

Utility Theory (Contd)

U(W)

Risk Taker

W

U(W)

Risk Neutral

W

3

Utility Theory (Contd)

Assume the following Utility function U(w)

2w - 0.01w2 where w represents change in

Wealth. Prob Stock A Stock B 0.30

19 64 0.40 64 51 0.30 91 36 E(UA)

19x0.30 64x0.40 91x0.30

58.60 E(UB) 64x0.30 51x0.40 36x0.30

50.40 Choose A

4

Mean-Variance Criterion

(1) Investors are risk averse (2) Returns are

distributed normally, or investor Utility

functions are quadratic An investor will prefer

A to B if E(RA) gt E(RB) and ?A ? ?B or E(RA)

? E(RB) and ?A lt ?B

5

Return and Risk of a Portfolio

Expected return of a portfolio

Variance of a portfolio

Recommended