Example Exercise 2 PowerPoint PPT Presentation

1 / 13

Title: Example Exercise 2

1

Example Exercise 2

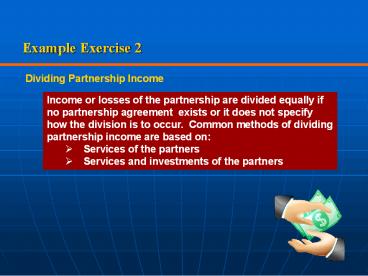

Dividing Partnership Income

- Income or losses of the partnership are divided

equally if no partnership agreement exists or it

does not specify how the division is to occur.

Common methods of dividing partnership income are

based on - Services of the partners

- Services and investments of the partners

2

Example Exercise 2

Services of Partners

One method of dividing partnership income is

based on the services, called salary allowances,

by each partner to the partnership. Since

partners are not employees, these allowances are

recorded as divisions of net income and are

credited to the partners capital accounts.

3

Example Exercise 2

Services of Partners

Assume that the partnership agreement of Jennifer

Stone and Crystal Mills provides for the

following division of net income

Net income for the current period is 150,000

4

Example Exercise 2

J. Stone C. Mills Total

Net income 150,000

Annual salary allowance 60,000 48,000 108,000

5

Example Exercise 2

J. Stone C. Mills Total

Net income 150,000

Annual salary allowance 60,000 48,000 108,000

Interest Allowance 19,200 14,400 33,600

6

Example Exercise 2

J. Stone C. Mills Total

Net income 150,000

Annual salary allowance 60,000 48,000 108,000

Interest Allowance 19,200 14,400 33,600

Remaining income 8,400

7

Example Exercise 2

J. Stone C. Mills Total

Net income 150,000

Annual salary allowance 60,000 48,000 108,000

Interest Allowance 19,200 14,400 33,600

Remaining income 4,200 4,200 8,400

8

Example Exercise 2

J. Stone C. Mills Total

Net income 150,000

Annual salary allowance 60,000 48,000 108,000

Interest Allowance 19,200 14,400 33,600

Remaining income 4,200 4,200 8,400

83,400 66,600 150,000

9

Example Exercise 2

2

Steve Prince Chelsy Bernard Total

Net income 240,000

Annual salary allowance 42,000 0 42,000

10

Example Exercise 2

2

Steve Prince Chelsy Bernard Total

Net income 240,000

Annual salary allowance 42,000 0 42,000

Interest 1,800 13,500 15,300

11

Example Exercise 2

2

Steve Prince Chelsy Bernard Total

Net income 240,000

Annual salary allowance 42,000 0 42,000

Interest 1,800 13,500 15,300

Remaining income 91,350 91,350 182,700

12

Example Exercise 2

2

Steve Prince Chelsy Bernard Total

Net income 240,000

Annual salary allowance 42,000 0 42,000

Interest 1,800 13,500 15,300

Remaining income 91,350 91,350 182,700

Net income 135,150 104,850 240,000

13

Example Exercise 2

2

2

2A, 2B

? For Practice PE 2A, PE 2B

Recommended