Disco Views of the Future: Threats PowerPoint PPT Presentation

1 / 16

Title: Disco Views of the Future: Threats

1

2

3

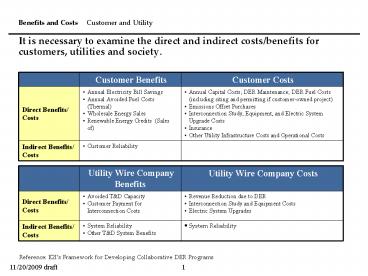

4

5

6

7

Disco Views of the Future Threats

Opportunities

Disco Role in Distributed Resources

- No sources of new revenue

- More responsibilities without due compensation

- Continual cost cutting

- Competitive bypass

- New revenue sources

- Positive stakeholder relations

- Significant investment

- Reduction of social obligations

CROSSED WIRES SCENARIOS FOR THE FUTUREOF THE

ELECTRICDISTRIBUTION BUSINESS XENERGY Scenario

Workbook

Source Crossed Wires, XENERGY Electric

Distribution Business Study (EDB)

8

Disco Views of the Future (selected) -- from

XENERGY Crossed Wires Study

Disco Role in Distributed Resources

- Distribution will continue to be a monopoly, but

with the risk of by-pass. - Competition customer choice will continue to

expand, but - 10 years from now, the regulated company will

still be responsible for a large share of the

load, and power cost adjustment clauses will be

the norm. - Regulated distribution companies will own DG

storage devices on their systems in 5 years. - Virtually all customers will be under time-of-use

pricing and metered hourly. - Technology will be more intelligent on both sides

of the meter

Source Crossed Wires, XENERGY Electric

Distribution Business Study (EDB)

9

wires.net - 1 of 4 Future Scenarios

Disco Role in Distributed Resources

- In this future, technology advances result in

lower costs and substantially improved prospects

for distributed generation and electricity

storage. - These new technologies appeal strongly to

consumers, since they offer an economic

alternative to central power production. - These alternative technologies finally become

disruptive enough to the electric distribution

business that the need for traditional regulation

is challenged. - As DP begins to increase its market share, discos

recognize for the first time a real threat to the

monopoly franchise. - Such competitive threats simultaneously spark new

technology innovations in power delivery and in

central plant production. - With full competition, the marketplaceinstead of

regulatorsbegins to sort out - where distributed generation makes the most

sense, and - where network service continues to be the most

economic means to provide electric service to

customers.

10

wires.net Scenario

Disco Role in Distributed Resources

Source Crossed Wires, XENERGY Electric

Distribution Business Study (EDB)

11

wires.net Scenario

Disco Role in Distributed Resources

Source Crossed Wires, XENERGY Electric

Distribution Business Study (EDB)

12

MA PV Potential Only Federal/State Incentives

Option 3 Assumptions

Residential

Commercial

Size (kWpac)

2.5

250

Tax Credits ()

15 Up to 1,000 max.

10 ITC

13

MA PV Potential Maximum Incentives

Option 1 Assumptions

Residential

Commercial

Size (kWpac)

2.5

250

MTC Buydown (/kW)

3,500

2,800

Mainstay ERP (/kW)

150

150

Tax Credits ()

15 Up to 1,000 max.

10 ITC

14

MA CHP PV Potential Low case scenario

Low Case for Massachusetts CHP PV Market

Potential (MW)

MW

15

MA CHP PV Potential High case scenario

High Case for Massachusetts CHP PV Market

Potential (MW)

MW

16

Green Buildings Program Framework

A 25-35 million, 5-year commitment to DG /

Energy Efficiency. At least 50 directed to PV.

Market-Driven Open to all technologies

MTC-Determined

- Feasibility Studies

- Competitive Solicitations

- Roughly 10 of annual budget

- Partnerships

- Tailor to maximize public benefit

- Roughly 45 of annual budget

1

Green Schools

Affordable Green Housing

Utility Congestion Relief

- Installation Incentives

- RE component EE component (CII)

- Matrix with low base incentive by tech

- Additional funds for priority targets

- Predictable declining subsidy over time

- Rolling process for small installations

- Competitive for large installations

- Roughly 45 of annual budget

3

2

Recommended