Marital Dissolution Stock Redemption PowerPoint PPT Presentation

1 / 11

Title: Marital Dissolution Stock Redemption

1

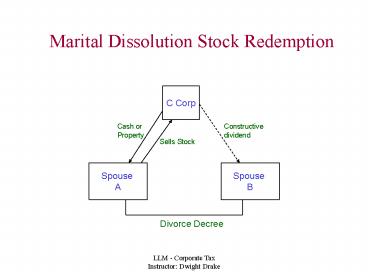

Marital Dissolution Stock Redemption

C Corp

Cash or Property

Constructive dividend

Sells Stock

Spouse A

Spouse B

Divorce Decree

2

Final Regs Under 1041

Issue If redemption part of divorce, what is

relationship of 1041 (no gain or loss on divorce

property division) and 302 redemption

provisions? Reg. 1.1041-2(c) If

redemption for benefit of non-transferring spouse

under primary and unconditional obligation

standard, then - No gain or loss to

transferring spouse per 1041. -

Constructive dividend to non-transferring

spouse. If primary and unconditional

standard not met for constructive dividend, then

1041 not apply and transferring spouse must

recognize gain or loss. Parties may elect

opposite rule to one that would otherwise apply

if they both agree. Bottom line No

opportunity to whipsaw and both avoid tax.

3

Problem 282

- Basic Facts P owns 25k of F Corp 100k

outstanding common shares. FMV stock 2.5 mill

(100 per share) basis 25k. Mucho E P. F

Corp has right of first refusal. P wants to give

100k to alma mater SU. - F Corp distributes 100k to P in redemption of

1000 shares P gives cash to SU. 100k dividend

because not qualify under 302(b) series. P has

100k dividend income and 100k charitable

contribution, subject to 170 deduction

limitations. - P gifts 1000 shares to SU and F Corp redeems from

SU for 100k two months pursuant to oral

understanding. SU under no obligation. If no

obligation (just oral understanding), no

constructive dividend to P per Grove and Rev.

Rule 78-197. P has 100k charitable contribution

deduction and no income. - Same, except P gives 250 shares a year for four

years and SU always redeems. Still OK under

Grove if SU not obligated, but pattern is riskier

suggests deal.

4

304 Brother-Sister Redemptions

- 304 impact

- - A redemption tested by B

- ownership change.

- If 301 distribution, first A EP,

- then B EP.

- If 301 distribution, deemed 351

- transfer to A, followed by A

- redemption of hypothetical

- shares.

- 304 trumps 351 boot rule if

- stock and property actually

- transferred by A. Not so for

- acquisition debt.

- - Corporate 50 318 factor reduced to 5.

A Corp

B Corp

B Corp Stock

Cash or Property

Common Owner 50 of both

5

304 Parent-Sub Redemptions

- 304 impact

- - A redemption tested by B

- ownership change.

- If 301 distribution, first A EP,

- then B EP.

- - 304 trumps 351 boot rule if

- stock and property actually

- transferred by A. Not so for

- acquisition debt.

- - Corporate 50 318 factor reduced to 5.

A Corp

B Corp

50 Owned

B Corp Stock

Cash or Property

50 owned

Stock Owner

6

Problem 295 - 2

- Basic Facts B Corp has 100 shares outstanding

no EP. O Corp has 100 shares outstanding 5k

accumulated EP. C owns 80 shares of B Corp

(basis 40k) and 60 shares of O Corp (basis 9k). - C sells 20 O Corp shares (basis 3k) to B Corp for

4k. - - Since C has control of both corps (at

least 50 voting), 304(a)(1) treats as

constructive redemption of B corp stock tested by

Cs holding in O Corp stock. Percentage in O

Corp 60 before and 56 after (40 direct and 16

via B Corp). Hence, C deemed to have received

301 distribution from B Corp. - - Distribution first out of B Corp EP

(0), then O Corp EP. Hence, 4k dividend under

301. O Corp EP reduced to 1k. - - C basis in B Corp stock increase 3k

(basis in O corp transferred shares) to 43k, as

if 351 transaction. B corp basis in O Corp

transferred stock 3k (transferred basis) per 362,

as if 351 transaction.

7

Problem 295 - 2

Basic Facts B Corp has 100 shares outstanding

no EP. O Corp has 100 shares outstanding 5k

accumulated EP. C owns 80 shares of B Corp

(basis 40k) and 60 shares of O Corp (basis

9k). (b) C sells 20 O Corp shares (basis 3k) to

B Corp for 3k cash and I share B stock (FMV 1k).

- Since C has control of both corps (at

least 50 voting), 304(a)(1) treats as

constructive redemption of B corp stock tested by

Cs holding in O Corp stock. C would like to

claim straight 351 deal with 3k boot and 1k gain

(4k minus basis of 3k. Not so because

304(b)(3)(A) says 351 applies only to

stock-for-stock portion of exchange, not boot.

304(a) governs boot. - Here 3k deemed

redemption of B Corp stock tested by Cs holdings

in O Corp. As in (a), clear 301 dividend of 3k,

which reduce O Corp EP.

8

Problem 295 - 2

Basic Facts B Corp has 100 shares outstanding

no EP. O Corp has 100 shares outstanding 5k

accumulated EP. C owns 80 shares of B Corp

(basis 40k) and 60 shares of O Corp (basis

9k). (c C sells 20 O Corp shares (basis 3k)

to B Corp for 1 share B stock (FMV 1k) and O Corp

takes stock subject to 3k debt C incurred to buy

stock. - 304(b)(3)(B) exception says

304(a) not apply to liability assumed or taken

subject to in 351 transaction if liability

incurred by transferor to acquire stock.

- So here straight 351 transaction. Per 357,

liability transfer does not trigger any gain or

loss (not in excess of basis). C basis in 1

share of B Corp stock received is zero (3k basis

in O Corp stock transferred less 3k debt

transferred) per 358(d).

9

Problem 295 - 2

- Basic Facts B Corp has 100 shares outstanding

no EP. O Corp has 100 shares outstanding 5k

accumulated EP. C owns 80 shares of B Corp

(basis 40k) and 60 shares of O Corp (basis 9k). - C sells all 60 O Corp shares (basis 3k) to B

Corp for 12k cash. - - Since C control both (50 plus voting

stock), deemed redemption from B Corp to C tested

against O Corps percentages before and after.

Before percentage was 60 after is 48

(attribution from B Corp). No hope under

302(b)(2) because not less than 80. May have

good (b)(1) not essentially equivalent to

dividend argument because now under 50. - - Query impact of B Corp (controlled by

C) controlling now O Corp. Does this wipe out

(b)(1) hope? Probably not. - - If valid exchange, not 301 dividend, C

has 3k LTCG (12k minus 9k basis). Cs B corp

basis not effected.

10

303 Redemption

Purpose Permit exchange treatment on

redemption of stock included in dead persons

estate that otherwise would be 301 dividend

distribution to pay estate and inheritance taxes

and funeral and administrative expenses.

Requirements - Timing Pay within 90 days

of estate tax assessment period, 60 days after

Tax Court determination, of 6166 installment

period. Distributions after 4 yrs limited to

lesser of unpaid qualified items just before

distribution or qualified items paid within one

year of distribution. - 35 Test FMV of

stock must exceed 35 of gross estate less 2053

and 2054 deductions (debts, expenses and

losses). - If own 20 or more of multiple

corps, can aggregate for 35 test. Spouse

interest in community property or jointly owned

stock included for 20 test but not 35 test.

11

Problem 297

Basic Facts G dies Gross estate 2 mill 100k

estate taxes and burial and administration

expenses Estate includes 200k FMV X Corp stock

(total o/s FMV 1.4 mill) and 400k FMV Y Corp

stock (total o/s FMV 1.6 mill). G wife A owns

200k X Corp stock, which she held as

tenant-in-common with G. Will Y Corp redemption

qualify for 303 treatment? - 303 requirement is

over 35 of gross estate less allowable

deductions (here 1.9 mill). 35 is 665k. - Y

stock of 400k isnt enough. X stock in estate

can be aggregated if estate owns 20 or more of

all classes of stock of both entities. Wife As

tenant-in-common shares may be included for 20

test, but not 35 test. With Wife As shares,

20 test met for both X and Y, so can consider

both. - But 35 test still failed because

value of X and Y stock in estate only 600k, not

665. Hence, 303 redemption treatment not

available.

Recommended