BASIC BOND VALUATION MODEL PowerPoint PPT Presentation

1 / 43

Title: BASIC BOND VALUATION MODEL

1

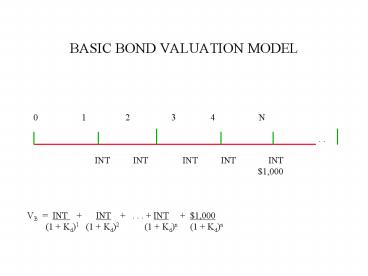

BASIC BOND VALUATION MODEL

0 1 2

3 4 N

. .

INT INT INT INT

INT

1,000

VB INT INT . . . INT

1,000 (1 Kd)1 (1 Kd)2

(1 Kd)n (1 Kd)n

2

THINGS THAT AFFECT BOND VALUE

- ANYTHING THAT AFFECTS (CHANGES) Kd

- E.G., CHANGING INFLATION EXPECTATIONS, CHANGES IN

THE REAL RATE (K), CREDIT RISK, LIQUIDITY,

MATURITY RISK.

3

BASIC BOND VALUATION MODEL

0 1 2

3 4 N

. .

INT INT INT INT

INT

1,000

VB INT INT . . . INT

1,000 (1 Kd)1 (1 Kd)2

(1 Kd)n (1 Kd)n

4

VB INT(PVIFA, N, Kd) 1,000(PVIF, N, Kd)

5

SIMPLE EXAMPLE ASSUMING ONE INTERESTPAYMENT PER

YEAR

PAR VALUE 1,000 (DOESNT CHANGE) COUPON RATE

12 (DOESNT CHANGE) INTEREST 1,000 X 12

120 (DOESNT CHANGE) YIELD (Kd) 12 (DOES

CHANGE) MATURITY 10 YEARS (DOES CHANGE) VB

INT(PVIFA, N, Kd) 1,000(PVIF, N, Kd)

120(PVIFA, 12, 12) 1,000(PVIF, 12, 12)

1,000

6

CALCULATOR PROCEDURE USING TVM BUTTONS

- SET P/Y 1

- ENTER 10 FOR N

- ENTER 120 FOR PMT

- ENTER 1,000 FOR FV

- ENTER 12 FOR I/Y

- CPT PV 1,000

7

VB PAR VALUE

WHEN Kd COUPON RATE

8

VB? NOT EQUAL PAR VALUE

WHEN Kd IS NOT EQUAL TO COUPON RATE.

9

AS Kd RISES

- BOND VALUES FALL

- VB INT INT . . . INT

1,000 - (1 Kd)1 (1 Kd)2 (1 Kd)n

(1 Kd)n

10

EXAMPLE WITH YIELD RISING

PAR VALUE 1,000 COUPON RATE 12 INTEREST

1,000 X 12 120 YIELD (Kd) 16 MATURITY

10 YEARS VB 120(PVIFA, 10, 16) 1,000

(PVIF, 10, 16) 806.67 (LESS THAN

1,000 SELLS AT A

DISCOUNT FROM PAR)

11

AS Kd FALLS

- BOND VALUES RISE

- VB INT INT . . . INT

1,000 - (1 Kd)1 (1 Kd)2 (1 Kd)n

(1 Kd)n

12

EXAMPLE WITH YIELD FALLING

PAR VALUE 1,000 COUPON RATE 12 INTEREST

1,000 X 12 120 YIELD (Kd) 8 MATURITY

10 YEARS

VB 120(PVIFA, 10, 8) 1,000(PVIF, 10, 8)

1,268.40 (MORE THAN 1,000 SELLS

AT A PREMIUM TO PAR)

13

A BONDS PRICE APPROACHES ITS PAR VALUE AS BOND

APPROACHES MATURITY

BOND PRICE

PATH OF PREMIUM BOND

1,000

PATH OF A DISCOUNT BOND

TIME

14

FINDING A BONDS YIELD (Kd), GIVENITS PRICE (VB)

PAR 1,000 COUPON RATE 8 PRICE 701.22 N

20 Kd ?

701.22 80 80 . .

. 1,080 (1 Kd)1 (1

Kd)2 (1 Kd)20

15

CALCULATOR APPROACH

701.22 80(PVIFA, 20, Kd) 1,000(PVIF, 20,

Kd)

-701.22 PV 80 PMT 20 N 1,000 FV CPT I/Y

12

16

INTEREST RATE RISK

- THE RISK THAT A BONDS PRICE WILL FALL BELOW ITS

PAR VALUE BECAUSE OF A RISE IN INTEREST RATES. - THE MORE DISTANT A BONDS MATURITY, THE GREATER

ITS EXPOSURE TO INTEREST RATE RISK.

17

INTEREST RATE RISK EXAMPLE

PAR 1,000 COUPON RATE 10 (ANNUAL)

BOND VALUES Kd

2 YEAR BOND 20 YEAR BOND 6

1,073.34

1,458.80 8 1,035.67

1,196.36 12

966.20

850.61 14 934.13

735.07 16

903.67 644.27

18

FINDING BOND VALUES IN THE REALWORLD USING

SEMIANNUAL COMPOUNDING

- VB INT/2 INT/2 . . .

INT/2 1,000 - (1 Kd/2)1 (1 Kd/2)2

(1 Kd/2)nx2 - P/Y 2

- VB INT/2(PVIFA, 2N, Kd) 1,000(PVIF, 2N,

Kd)

19

EXAMPLE OF BOND VALUATION WITHSEMIANNUAL

COMPOUNDING

PAR VALUE 1,000 COUPON RATE 8 Kd 12 N

20 VB 80/2(PVIFA, 2X20N, 12/2) 1,000(PVIF,

2X20N, 12/2) 699.07

20

FINDING BOND YIELDS WITH SEMIANNUALCOMPOUNDING

- VB INT/2 INT/2 . . .

INT/2 1,000 - (1 Kd/2)1 (1 Kd/2)2

(1 Kd/2)n

PAR VALUE 1,000 COUPON RATE 8 Kd ? N

20 VB 699.07

21

EXAMPLE FINDING BOND YIELDS WITH SEMIANNUAL

COMPOUNDING

699.07 80/2(PVIFA, 2X20N, Kd/2) 1,000(PVIF,

2X20N, Kd/2)

SDT 1.0196 CPN 8 RDT 1.0116 RV100 360 2/Y P

RI 69.907 YLD CPT 12

22

PREFERRED STOCK

- HAS ELEMENTS OF BOTH STOCK AND BONDS

- FIXED NON TAXDEDUCTIBLE DIVIDENDS

- CAN BE SKIPPED

- ALL PREFERRED DIVIDENDS IN ARREARS MUST BE PAID

BEFORE COMMON STOCK DIVIDENDS PAID

23

PREFERRED STOCK

VALUED AS A CONSTANT STREAM OF PAYMENTS OR AS A

PERPETUITY PVPS DPS KPS IMPLIES

KPS DPS PVPS

24

PREFERRED STOCK EXAMPLE

KPS 12 DPS 8 PVBS 8/.12 66.67

25

COMMON STOCK

- DIVIDENDS BY COMPANY OPTIONAL

- DIVIDENDS CAN VARY

- VALUATION DEPENDS ON ASSUMPTION OF CONSTANT

GROWTH OF DIVIDENDS

26

COMMON STOCK CASH FLOWS

0 1 2 3

- ?

. . . .

D0 D1 D2

D3

P0 D1 D2

D3 . . . (1 Ks)1 (1

Ks)2 (1 Ks)3

(NOT PRACTICAL)

27

TO PERMIT COMMON STOCK VALUATION,ONE OF TWO

ASSUMPTIONS MUST BE MADE

- DIVIDEND GROWTH IS ZERO (AS FOR PREFERRED STOCK)

OR - DIVIDEND GROWTH IS CONSTANT

28

CONSTANT GROWTH MODEL AKAGORDON GROWTH MODEL

- ASSUMES DIVIDENDS GROW AT A CONSTANT RATE

- VALUES DIVIDENDS AT THE START OF CONSTANT GROWTH

- THE START OF CONSTANT GROWTH CAN OCCUR ANY TIME

29

CONSTANT GROWTH EQUATION

P0 Dg(1 g) Ks - g Ks gt g

DEFINE TERMS

DISCUSS IMPLICATIONS

30

CONSTANT GROWTH EXAMPLE

D0 2 Ks 10 g 8 CONSTANT GROWTH

STARTS AT TIME ZERO P0 2(1 .08) 108

.10 - .08

31

CONSTANT GROWTH MODEL WITHSUPERNORMAL GROWTH

ASSUMES NONCONSTANT HIGH GROWTH IN EARLIER YEARS,

THEN CONSTANT GROWTH THEREAFTER

0 1 2

3

4

g1

g2

g3

g3

g3

. . .

32

EXAMPLE SUPERNORMAL GROWTH

- YOU ARE CONSIDERING THE PURCHASE OF AN IPO CALLED

COMPUTER SOFT, INC. - EARNINGS AND DIVIDENDS EXPECTED TO GROW AT 20

DURING YEAR 1, 15 DURING YEAR 2, AND 12

THEREAFTER. - D0 1.50 Ks 15

33

SUPERNORMAL GROWTH EXAMPLE

0 1 2

3

20

15

12

12

1.50

1.80

2.07

2.32

1.50(1.2)

1.8(1.15)

2.07(1.12)

1.80 2.07

2.32/(.15 - .12) P0 (1.15)1

(1.15)2 (1.15)2

61.61

34

A BRIEF LECTURE ON THE TERM STRUCTURE OF INTEREST

RATES

Term structure a schedule showing the yields on

securities alike in

all respects except their term to

maturity.

Example

U.S. Treasury Bonds

Years to maturity Yield 1

5 2

5.5 3

6

35

Yield Curve

The graph of the term structure is called the

yield curve

.

Yield

.

6 5.5 5

.

years

1 2 3

36

Shape of the Yield Curve

The yield curve can be positively sloped, flat or

negatively Sloped. Positive implies

short-term rates are expected to rise Flat

suggests no change in short-term rates Negative

short-term rates are expected to fall

37

Theories explaining the shape of the yield curve

- Expectations Hypothesis

- Market Segmentations Hypothesis

- Liquidity Preference Hypothesis

38

Expectations Hypothesis

Says spot rates are the average of expected

future Short-term rates. A spot rate is a rate

observable on a security today Example of spot

rates Yield on a one year bond 5

Yield on a two year

bond 5.5

Yield on a three year bond 6

39

Rationale behind the Expectations Theory

The Expectations theory is based on the notion

that when Investing over a period greater than

one year, investors Have a choice of investing in

a long-term bond or a series Of one year bonds.

For investors to be indifferent between This

choice, long-term rates have to be equal to the

average Of the expected future short-term rates

on the one year bonds.

40

Mathematical Rationale

(1 rn)n (1 r1)(1 r2)(1 r3) . . .(1

fn)

41

Alternatively . . .

(1 rn)n (1 rn-1)n-1(1 fn) This

implies (1 rn)n fn

-1 Using this

equation (1 rn-1)n-1

we can solve for the

forward rate

42

Example

0 1 2 3 4

10

12

The yield on a 4 year Treasury bond is 12 The

yield on a 3 year Treasury bond is 10 Find the

expected one-year rate during year 4 f4

(1.12)4 -1 1.5735 -1

18.22 (1.10)3

1.3310

43

Market Segmentations Hypothesis

The theory that investors and borrowers have

preferred maturity Habitats. The yield curve is

thought to be determined by the Demand-supply

relationship within each habitat

44

Liquidity Preference Hypothesis

Assumes the yield curve is upward sloping

(usually) because Investors would rather lend

short-term and borrowers would Rather borrow

long-term

Recommended