Lecture 4 - Monte Carlo improvements via variance reduction techniques: antithetic sampling - PowerPoint PPT Presentation

Title:

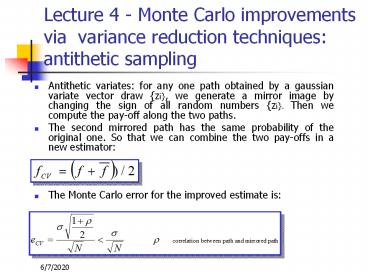

Lecture 4 - Monte Carlo improvements via variance reduction techniques: antithetic sampling

Description:

Lecture 4 - Monte Carlo improvements via variance reduction techniques: antithetic sampling ... In the standard Monte Carlo the error decreases slowly, as 1 ... – PowerPoint PPT presentation

Number of Views:1035

Avg rating:3.0/5.0

Title: Lecture 4 - Monte Carlo improvements via variance reduction techniques: antithetic sampling

1

Lecture 4 - Monte Carlo improvements via

variance reduction techniques antithetic

sampling

- Antithetic variates for any one path obtained by

a gaussian variate vector draw zi, we generate

a mirror image by changing the sign of all random

numbers zi. Then we compute the pay-off along

the two paths. - The second mirrored path has the same probability

of the original one. So that we can combine the

two pay-offs in a new estimator - The Monte Carlo error for the improved estimate

is

2

Monte Carlo improvements via variance reduction

techniques control variates

- Control variates the Monte Carlo simulation is

carried out both for the original problem as well

as a similar problem for which we have a closed

form solution. Being - f the option value we want to estimate and

- y the analytical exact value of the auxiliary

option - an improved estimator of f is

- As a consequence of the above relations, control

variates become more and more efficient as the

auxiliary option is more correlated (or

anti-correlated) with the original option, i.e.

when the two problems are similar.

3

Monte Carlo improvements via variance reduction

techniques control variates and p

- Let us back to the problem of estimate p. A good

choice for a control variable is a polygon with n

edges inscribed in the circle. Indeed - a closed formula exists for any value of n

- it has an high superposition with the circle

Stochastic term

- The error scales again as 1/sqrt(N) but with a

smaller proportional constant

4

Monte Carlo improvements low discrepancy

sequences Quasi Monte Carlo

- In the standard Monte Carlo the error decreases

slowly, as 1/sqrt(N), with number of samples, N,

because draws do not fill in the space in a

regular way. Indeed some gaps are present

(clustering effects). - In low discrepancy sequences the points are

chosen in order to fill in the space more

regularly and uniformly, without inhomogeneities.

As a result the function to be integrated

converges not as one over the square root of the

number of samples (N) but much more closely as

one over N (Quasi Monte Carlo).

5

Monte Carlo improvements low discrepancy

sequences definition and results

- The most famous algorithms to generate low

discrepancy numbers are the Sobol and Halton

sequences. - The discrepancy is a measure of how inhomogeneous

a set of D-dimensional vectors of random numbers

fills in a unit hypercube. - By definition, in a low discrepancy sequence (in

D dimension), the discrepancy scales with the

number of draws, N, as

6

Monte Carlo improvements low discrepancy

sequences high dimensional behavior

- Pros For a given precision, a lower number of

scenarios are needed.

- Cons

- The convergence speed depends on problem

dimension (making the method inefficient in very

high dimensions). - Quasi Monte carlo simulation are not reliable

when high dimensions are involved, with a

breakdown of homogeneity along some hyper-planes.

7

Monte Carlo pros and cons

- Pros

- Can be used in high dimensional problems.

- Easy to implement

- Easily extensible to any type of pay-off

- Cons

- Heavy from a computational point of view.

8

Conclusion

- We have presented a powerful numerical technique

to price exotic options the Monte Carlo method. - Numerical methods in finance will become more and

more important due to the rapid growth in

financial markets of the exotic products, with a

clear trend to increase the complexity embedded

in the exotic options. - References P. Jackel - Monte Carlo Methods in

Finance, Wiley Finance, (2002).

Recommended

CrystalGraphics Presentations