FUTURES - PowerPoint PPT Presentation

Title:

FUTURES

Description:

DEFINITION Futures (forward) contracts are agreements between two agents where one agrees to purchase and the other to sell (deliver) a given amount of a specific ... – PowerPoint PPT presentation

Number of Views:104

Avg rating:3.0/5.0

Title: FUTURES

1

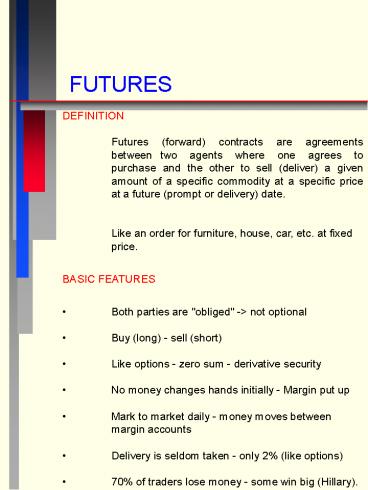

FUTURES

- DEFINITION

- Futures (forward) contracts are agreements

between two agents where one agrees to purchase

and the other to sell (deliver) a given amount

of a specific commodity at a specific price at a

future (prompt or delivery) date. - Like an order for furniture, house, car, etc. at

fixed - price.

- BASIC FEATURES

- Both parties are "obliged" -gt not optional

- Buy (long) - sell (short)

- Like options - zero sum - derivative security

- No money changes hands initially - Margin put up

- Mark to market daily - money moves between

2

FUTURES VS. FORWARD CONTRACTS

- FUTURES CONTRACTS ARE STANDARDIZED

- sold on exchanges - Chicago Board Trade (1848)

- involve clearing house

- trading in pit - no specialist - different

prices - FORWARD CONTRACTS ARE NOT STANDARDIZED

- sold over the phone (over the counter)

- no clearing house

- common for currency trading - banks

- 24 hour market

- no mark to market - end day settlement

- allow contingent delivery - sale of house etc.

- Look at Futures Quotes www.futures.quote.com

- QUESTION Which commodities are likely to have

- futures traded? (A commodity that can be

graded - standardized - widely used - volatile

price)

3

- In order to simplify things and focus on the most

important issues, I will assume futures and

forward prices are the same. - When the risk-free rate and any applicable

carrying cost rate is the same for all

maturities, then this is a reasonable assumption.

This is because the primary cash-flow difference

between comparable futures and forwards is the

marking to market for futures. - As long as the same rate applies, any

intermediate cash flows get invested at the same

rate so there is no advantage of one over the

other. However, if the futures price is

positively (negatively) correlated with interest

rates, then we will tend to reinvest gains at

higher (lower) rates of interest and futures will

have an advantage (disadvantage) over forwards.

Futures prices will therefore be higher (lower)

than forward prices. - Other reasons why comparable futures and forwards

may have different prices are tax, margin,

liquidity or transactions costs differences.

These are ignored here. - As long as the maturity of the contract is short,

even changing interest rates will have little

effect on futures versus forward prices.

4

Example Calculating returns on futures

-speculator

ASSUME - It is January - July wheat futures

sell for 4.84/bushel - Each contract covers

3000 bushels - Margin rate is 15 - Trading

commission is 30/roundtrip Buy 5

contracts Figure your investment 5 x 3000 x

4.84 x .15 (30 x 5) 11,040 A. Sell

your futures in April when price is 4.96 /

bushel .149/4 months or 44.8

annual B. Sell your futures in March when price

is 4.75/bushel -.136/3 months or

-54.3 annual

5

Hedging Locks in Profit - Eliminates Price Risk

- SIMPLE HEDGING EXAMPLE - Mortgages

- A local bank makes commitments with customers

for 5 million of mortgage loans today at a fixed

rate of interest. The mortgages are not actually

paid out until real estate closings in two

months. The banks funding costs are 4 m. - At the same time, an insurance company plans to

buy 5 million in mortgage-backed securities in

two months to support 6 million in insurance

premiums it will receive. - Local Bank - short hedger - hedges risk by

selling futures. - Insurance Company - long hedger - hedges by

buying mortgage futures. - Timing Local Bank Insurance Co

- now sell futures 5 buy futures -5

- 2 months later cost -4 gets premiums 6

- Net Profit 1 1

6

Price Changes Have No Net Impact

1. Suppose mortgage rates rise so the value of

the 5 million mortgages is 3 million in two

months. What happens? Local Bank

Insurance Co. Makes mortgages 3 Buys

mortgages -3 Buy back futures -3

Sell back futures 3 NET 0

0 What are the respective gains and losses for

the Bank and the Insurance Co.? Local

Bank Insurance Co. Loss on mortgages -2

Gain on mortgages 2 Gain on futures 2

Loss on futures -2 NET 0

0 2. Suppose mortgage rates fall so the

value of the 5 million mortgages is 6 million

in two months. What happens? Local

Bank Insurance Co. Makes mortgages 6 Buys

mortgages -6 Buy back futures -6 Sell

back futures 6 NET 0 0 What are the

respective gains and losses for the Bank and the

Insurance Co.? Local Bank Insurance Co. Gain

on mortgages 1 Loss on mortgages -1 Loss

on futures -1 Gain on futures

1 NET 0 0

7

Information in Futures Prices

Problem Suppose your company delivers oil to

customers at a fixed price of 1 per gallon. You

have an inventory of 1 million gallons and

storage capacity for 2 million gallons. Your

customers will be using 0.5 million gallons per

month over the next four months. It is January 1

and you observe the following set of prices for

spot oil and oil futures. Spot 0.90 per

gallon February 1.00 March 1.11 April 1.2

3 What is your strategy for purchasing the oil

you will need? If there are many firms in your

situation, how might spot and futures prices

change in the near-term? Problem Assume

everything above but you observe a new set of

prices for spot oil and oil futures. Spot 1.23

per gallon February 1.11 March 1.00 April

0.90 What is your strategy for purchasing the

oil you will need? If there are many firms in

your situation, how might spot and futures prices

change in the near-term?

8

Problem Assume everything above but you observe

a new set of prices for spot oil and oil

futures. Spot 1.40 per gallon February 1.30

March 1.20 April 1.10 What is your strategy

for purchasing the oil you will need? If there

are many firms in your situation, how might spot

and futures prices change in the near-term?

(something like this happened in New England in

January 2000.) Redo each problem and assume that

you have 2 million gallons in inventory. Note

Futures prices signal information to market

participants and different price patterns can

induce different behaviors from participants.

Behavior also differs depending on inventory

levels.

9

Pricing Futures

- Assume fixed supply and demand and no carrying

costs (including zero interest rate and zero

storage cost). - QUESTION What should be the relation between

spot - and futures price?

- Ft,T St

- t a point in time, say, now

- T future date beyond time t

- Ft,T futures price covering time t to time

T - St spot price at time t

- This must occur or else arbitrage is possible

because with fixed supply and demand, spot price

will be the same in each future period. - QUESTION If Ft,T gt St then what can you do to

earn a - risk free profit?

- Buy spot and store it. Short futures and deliver

in the future to earn profit equal to (Ft,T -

St).

10

2. Relax assumption of zero carry costs A.

INTEREST CARRY COSTS Suppose interest rates are

positive, then interest payments make holding a

commodity (which pays no interest) less

attractive. It makes futures contracts more

attractive. This is like options where the

option price depends upon interest rates because

the value of competing positions depend on

interest rates. Thus with continuous

interest Ft,T Ster(T-t) B. For any

other carry costs we simply add a new term to the

exponent. For example, it costs something to

store the commodity such as grain silos,

insurance, etc. Assuming carry costs in

percent C and accrue continuously, then we

have the following Ft,T Ste(rc)(T-t)

(If the present value of storage cost is a

fixed C per unit of the commodity then Ft,T

(St C)er(T-t) ). C. There can also be a

benefit to holding an asset or commodity called a

convenience yield (Y) (e.g., dividend, coupon

payment, stock-out costs avoided) so that Ft,T

Ste(rc-Y)(T-t)

11

3. Interest rates for the futures contract life

are easy to observe but some carry costs and

convenience yield are difficult to estimate and

often vary over time. For example, if there is

uncertainty about whether war will break out in

the Middle East, the futures market may price in

a large convenience yield for oil futures.

However, if some believe that demand will fall if

OPEC cuts off supply, then U.S. oil buyers may

not believe that there should be much of a

convenience yield. 4. Synthetic futures assume

that there are no carry costs except interest

then we can show how to price futures using a

replicating portfolio composed of options.

Suppose we buy a call on a commodity with an

exercise price of Ft,T (the current futures

price) priced at Ct and sell a put with the same

exercise and maturity (T) priced at Pt. Assume

that the spot price of the commodity is St. This

portfolio has the same payoff at maturity as a

futures contract if the spot price rises above

(falls below) the exercise price, then we gain

(lose) dollar for dollar. Then from Put-Call

parity we must have Ct Pt St - Ft,Te-r(T-t)

We know that the the futures contract price is

set such that there is no initial investment

(ignoring the margin), therefore, Ct Pt St -

Ft,Te-r(T-t) 0 gt Ft,T Ster(T-t) which is

the correct pricing formula.

12

RELAX THE FIXED SUPPLY/DEMAND ASSUMPTION

- 4. Now the expected future spot price, which

depends on - expected future supply and demand, is important

- If the expected future spot is lower than the

present spot price and there are costs of carry

then the futures will be priced according to the

expected future spot price. - If the expected future spot is higher than the

present spot price then the futures will be

priced according to the present spot plus carry

costs. - One can always carry the commodity from the

present into the future but you can't pull it

back from the future. - The general pricing relationship is then

- Ft,T MinEt(ST), Ste(rc-Y)(T-t)

- QUESTION What are examples of each alternative

- pricing method?

- Perishables - Strawberries, milk

13

QUESTION How should zero coupon T-bond futures

be priced? QUESTION How should coupon T-bond

futures be priced? QUESTION How should SP

500 futures be priced? NOTE The futures price

does not include the expected return of the SP

over the contract period. This is because, if you

buy a contract you buy the systematic risk of the

SP and should be rewarded, that is Ft,T lt

Et(ST). - the seller is selling the risk and

the buyer buys it, so the buyer must be

compensated by paying a low Ft,T now and

expecting to receive a higher Et(ST) later.

14

The SP 500 futures price is not set at Et(ST)

because Ste(rc-Y)(T-t) lt Et(ST) ACCORDING TO

THE FUTURES PRICING MECHANISM, WE GO WITH THE

LOWER PRICE. If the market expects an extra

return in the SP beyond its normal expected

return required for its risk then both St and

Ft,T will move up to discount the extra no-risk

return and thus the relationship Ft,T

Ste(rc-Y)(T-t) still holds.

15

Another way to see that the futures price for

risky assets such as the SP 500 will be below

the expected future spot price is to assume that

the asset price grows at the assets expected

return k, which exceeds the risk-free rate r.

Assume there are no carry costs or dividends. A

speculator who buys the futures contract on the

asset and invests the present value of the

futures price in the risk-free asset has the

following cash flows Time t -Fe-r(T-t) put

money in risk-free investment now which will

be used to pay for the asset delivered on the

futures contract. Time T ST pay future spot

price on futures contract when futures mature

at time T. The expected net present value of this

investment must be zero given that both

investments are discounted at the appropriate

rates -Fe-r(T-t) ESTe-k(T-t) 0 Or F

ESTe(r-k)(T-t) Clearly, for any risky asset,

k gt r so that the futures price is always less

than the expected future spot price EST. Only

if the asset is risk free will the futures price

equal the expected future spot price.

16

Time Series Behavior of Futures Prices

Samuelson (1965) showed that futures prices will

fluctuate randomly over time and that the

variance of futures prices may not be constant

over time. He assumes that St1 aSt et , a

lt 1 This simple autoregressive model says that

the spot price of the asset is expected to

decline over time. Nevertheless, the variance of

the expected spot price increases over time

because the error terms can accumulate over time

and leave the realized spot price far from its

expected value. Even though the spot price

changes in a known way, the futures price

(assumed to be the expected spot price at

delivery) is not expected to change. It already

reflects the expected spot changes over time

defined by the model above. At each point in

time, we know what St is and with the model above

we know what the expected future spot price is

(say for 2 periods ahead we have a2ESt). Past

errors feed in to determine St but the past

pattern of spot prices is irrelevant, only the

present spot price is relevant. Futures price

depends on it according to the model. The

variance of the futures price usually increases

as a contract approaches maturity. This is

because a futures contract for delivery far in

the future will have a price very close to that

determined from the model above. Even if we get a

large positive (negative) error this period that

makes St1 much larger (smaller) than expected,

it will likely be offset by opposite sign errors

over the numerous future periods. Also, if a is

small, then future spot price is likely to be

small far in the future no matter what the error

is in any near-term period.

17

The error wont change our expectation for prices

far in the future because it is likely that the

error will be offset by other errors of the

opposite sign over time. However, if we get a

large error today, the near-term contracts have

little time left for other errors to offset a

recent large error. (this is similar to

Carmelos result that the discount rate for a

cash flow to be receive far in the future should

be about the risk-free rate until enough time

passes so that it starts to take on more

potential variance and risk) This example is one

way to show that there is not necessarily a

relationship between todays spot price and

todays futures price. Todays spot price depends

on what is happening today and todays futures

price depends mostly on what is expected to

happen well into the future at the delivery

date. Only if there is a link between the present

and the future will we see a link between spot

and futures prices. For example, oil prices may

be low today but if we know that war is likely to

break out in the Middle East in 6 months, then

the six month futures contract price will be

high. If people prepare for this possibility by

hoarding oil now, the present spot price will

also be high. If they dont hoard, then spot

prices may stay low. See oil or gas prices for

short and long contracts at cmegroup.com or

futures.quote.com.

18

EXAMPLE TESTING SP FUTURES FOR ARBITRAGE

OPPORTUNITIES

Spot SP Nov. 6, 2001 1118.86 Futures

Dec. 2001 1121.00 Mar.

2002 1122.40 SP dividend yield 1 2 month

Tbill rate 1.7 5 month Tbill rate

1.8 Prompt date is the Thurs. before the third

Friday of Month Theoretical Price

Actual - Theoretical FN,D 1118.86e(.017 -

.01)(44/365) 1119.80

1121 1119.80 1.20 FN,M 1118.86e(.018 -

.01)(128/365) 1122.00 1122.4

1122 0.4 There are only slight differences

between actual and theoretical futures prices. It

would probably not pay to try to arbitrage since

trading commissions may exceed profits. Assuming

no cost to trade then for the December

contract Arbitrage opportunity - sell futures /

buy spot Sell futures now/ make delivery in

Dec. 1121 Buy spot now

-1118.86 Forgo interest on funds

(1118.86e.017(43/365) 1) -2.24

Receive dividends (1118.86e( .01)(44/365)

1) 1.30 Guaranteed profit no matter what

SP does 1.20

19

Hedging With Futures

- When a futures contract on the exact commodity is

available then hedge ratio is 1 to 1. - 1 million bushels of 5 wheat -gt 1 million

bushels in futures - When a futures contract on a similar or related

commodity exists then calculate a hedge ratio. - For an effective hedge we want the change in the

value of the spot commodity to be equal to minus

the change in the value of the futures. The

amount of futures needed per unit of spot is - h hedge ratio - ?Spot price / ?Futures price

- - this means if the spot and futures price move

together (opposite), sell (buy) futures to hedge.

20

For example, suppose you hold IBM bonds but only

Treasury bond futures are available. You can

hedge your IBM position by knowing the change in

the price of your bond when the Tbond price

changes. Your bonds price change is (1) Py

Price of your bond Dury Duration of your

bond Yoy old yield of your bond Yny new

yield of your bond The Treasury bonds price

change is (2) PT price of treasury

bond DurT Duration of Treasury bond YoT Old

yield on Treasury bond YnT New yield on

Treasury bond

21

To get the hedge ratio divide (1) by

(2) Where h the units (dollars)

of futures to be sold per unit (dollar) of spot.

This is reliable in most cases less reliable if

durations change much with rate changes. It

assumes a parallel shift in yield curve. NOTE

This hedges only interest rate risk - default

risk is ignored.

22

EXAMPLECOMPLEX HEDGING - SOUTHEAST CORP

- 1. Assume that

- On Jan 6, 2001 Southeast authorized 60 million

of 25 year bonds to fund a building project which

would be needed in August 2001. - Bonds are Aa rated and have Yield of 12.88 if

issued today. - The bonds have a duration of 7.8

- A regression of Aa yield changes on Tbond yield

changes has a slope of 1.123 - The Tbond futures of September 2001 had a price

of 69 - 08 or 69.25 - The futures contract price is 69,250 on a

100,000 face value 8 contract - The cheapest to deliver bond for the September

contract has an 11.80 Yield. - It also has a duration of 8.5 years

23

FINDING THE NUMBER OF FUTURES CONTRACTS NEEDED TO

HEDGE

- FIND THE HEDGE RATIO

- h 7.8/8.5 x 1.123/1 x 1.118/1.1288 1.021

- FIND DOLLAR AMOUNT OF FUTURES NEEDED TO HEDGE

- F 60,000,000 1.021 61,260,000

- FIND NUMBER OF FUTURES CONTRACTS NEED

- NF 61,260,000/69,250 885

- Question How would we hedge a stock portfolio?

- You need the betas of the spot portfolio and the

futures - portfolio.

- h -Beta(Spot) / Beta(Futures)

24

International Finance and Foreign Exchange Futures

SIMPLE DEFINITION Buying one currency with

another INTEREST RATE PARITY - implies that all

countries have the same interest rate after one

adjusts up or down for the change in the

country's currency value. INTEREST RATES ARE

THE PRICE OF MONEY - Thus the futures price of,

say, the dollar in terms of the Euro, will depend

on their relative prices, i.e., the respective

interest rates. Ft,T the future price of one

unit of foreign currency in terms of the

domestic currency e.g, 2/1. St the spot

price of one unit of foreign currency in terms

of the domestic currency. Rd,T-t the domestic

interest rate covering the contract

period. Rf,T-t the foreign interest rate

covering the contract period. Ft,T Ste(Rd -

Rf)(T-t)

25

Like SP futures adjusted for dividends, here we

adjust for the rate earned on the foreign

currency. - if Rd Rf gt Ft St - if Rd gt

Rf gt Ft gt St - if Rd lt Rf gt Ft lt St You

can always exchange dollars for Euros and get

Euro interest rates so arbitrage forces interest

rates between countries to be the same adjusted

for expected currency depreciation or

appreciation. or, Ft,T / St e(Rd - Rf)(T-t)

Suppose Rd increases and Rf stays constant this

implies that Ft,T/St increases so St decreases or

Ft,T increases or both. WHAT OFTEN HAPPENS IS St

INCREASES BUT Ft,T INCREASES EVEN

MORE. QUESTION Why? ANSWER Because the spot

rate now will be a function of the expected

future spot rate - pure expectation

hypothesis investors hold currencies that they

expect to appreciate which increases the demand

for them now. Also, if a country increases its

interest rate (through the central bank),

investors might expect more increases and bid up

currency futures.

26

EXAMPLE OF INTEREST RATE PARITY AND EXCHANGE RATES

ASSUME Spot rate of British pound is 1.70 per

pound The annual pound interest rate is RL

.11 The annual dollar interest rate is

R .13 QUESTION What should be the Futures

price of pounds to be delivered in one

year? F 1.70 x e(.13 - .11)(1) 1.734

dollars per pound

27

Overall International

- Interest rate parity similar to PPP

purchasing power parity - International Cost of Capital Tom OBrien

- Lots of institutional details differences in

accounting, taxes, trade zones, tariffs, transfer

pricing, political risks, monetary and fiscal

policies, letter of credit, etc. - Hedging do shareholders expect a hedged cash

stream or an unhedged cash stream? - Revenues only foreign sales

- Costs only foreign production

- Profits Revenues Costs gt both foreign

- Assets only foreign plant

- Liabilities only foreign financing

- Equity Assets Liabilities gt both foreign

28

Steps in the 1997-1998Asian Financial Crisis

- Thailand experiences major financial collapse

- 2. Russia defaults on government debt

- 3. World-wide rush to buy U.S. Treasury bonds

(caused ITCM collapse Fed - banks - bail out). - 4. Dollar appreciates intermediate mechanism

- 5. Real U.S. export (import) prices increase

(decrease) - 6. U.S. exports (imports) fall (rise)

- 7. U.S. interest rates fall intermediate

mechanism - 8. U.S. consumption (savings) rises (falls),

investment rises

29

Graphing the relevant data for Asian Financial

Crisis

- Go to economagic.com, click on Federal Reserve,

St. Louis - 2. Click U.S. Balance of Payments Data

- 3. Click Balance on Current Account (this is

quarterly) - 4. Click Gif Chart or PDF Chart (see recent and

to 1960) - 5. Click Foreign Assets in the United States, Net

Capital Inflows (US Assets Abroad, Net Outflows) - 6. Click U.S. Interest Rate Data. Then click on

30-Year Treasury Constant Maturity or another

maturity - 7. Click Exchange Rate Data. Then click

Trade-Weighted Exchange Index Broad

30

8. For Export and Import Prices go to

www.bls.gov 9. Click Databases Tables tab 10.

Go to Prices International and click on Top

Picks 11. Select Imports All Comodities 12.

Select Exports All Comodities 13. Click

Retrieve Data. 14. Click Include Graphs and then

click Go. 15. Click More Formatting

Options. 16. Select 12-Month Percent Change and

Retrieve Data. 17. You can see that import

prices fell faster than export prices around

1997-1998.

Recommended

CrystalGraphics Presentations