Term Structure of Interest Rates: Relationship with the Business Cycle PowerPoint PPT Presentation

1 / 13

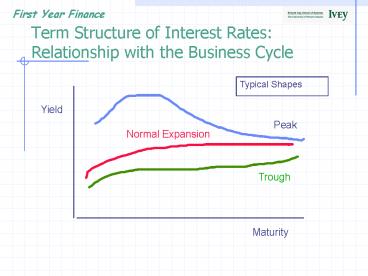

Title: Term Structure of Interest Rates: Relationship with the Business Cycle

1

Term Structure of Interest RatesRelationship

with the Business Cycle

Typical Shapes

Yield

Peak

Normal Expansion

Trough

Maturity

2

Short-Term Interest Rates Examples

- t-bill yield, e.g., 91-day rate ? issued by

government - bank rate ? central bank rate lending to banks

- bankers acceptance (BAs), e.g., 3-month ?

guaranteed by chartered banks - commercial paper, e.g., 3-month ? corporate

borrowing (typically unsecured) - prime rate ? chartered bank lending to best

customers - typically move together (but not lockstep)

- . . . Problem 1 and 3

3

Bonds Nomenclature

- A COUPON BOND is a combination of an annuity (the

annual or semi-annual coupon payments) and a zero

coupon bond (with face value due at maturity). - Example

- 15 year bond with 8 coupons (paid semi-annually)

and 1000 par value. - This coupon bond pays to the holder, 40 every

six months for fifteen years - At the end of fifteen years, the principal amount

of 1000 is repaid with the final coupon payment

of 40.

4

Zero Coupons Bond

- A ZERO COUPON BOND, only pays the holder the

principal or face value at maturity - No interim payments (or coupons) are due prior to

maturity, - At maturity the entire face value is repaid

- The holder will typically have purchased this

zero coupon bond for less than the face value - Quite simply, a zero coupon bond is a

- ZERO COUPON BOND

5

Zero Coupon Bonds Pricing

Price P (1r)T

- Where P is the bonds principle (or par value) due

upon maturity, r is the required return and T is

the time to maturity - Example 91-day T-bill with 100 par value. The

required return is 2 over this (one) 91-day

period

Price 100 98.04 (10.02)

6

Zero Coupon Bond Yields

- The yield to maturity (YTM) on a bond is simply

the IRR for the bond - Example

- The average bid price on 91-day T-bills is

98.352 (i.e., this is the price today for the

bills that will provide a cash flow of 100 in 91

days) - what is the YTM or IRR or T-bill rate?

7

Zero Coupon Bond Yields contd.

- NPV 0 -C0 C1/(1r)

- 0 -98.352 100/(1r)

- (1r) 100/98.352

- r 1.0168 1

- r .0168 or 1.68 which is a 91-day rate

- Using a spreadsheet

- RATE(1, 0, -98.352, 100) 0.0168

8

Zero Coupon Bond Yields contd.

- What rate would be quoted?

- By convention, annualize (using simple interest)

- 1.68 x (365/91) 6.72

- What is the effective annual rate of return?

- (1.0168)365/91 1 0.0691 or 6.91

9

Coupon Bond Pricing

Example 15 year bond with 8 coupons (paid

semi-annually) and 1000 par value. Suppose, the

required return is 5 every six months

Price 40 x 1- (1.05)-30 1000

846.28 0.05

(1.05)30

10

Coupon Bond Yields

- What is the YTM of a 2-year bond which has a

price today of 100 and pays semi-annual coupons

of 5 (i.e., has a coupon rate of 10)? - NPV 0 -C0 C1/(1r) C2/(1r)2

C3/(1r)3 C4/(1r)4 PRINC/(1r)4 - 0 -100 5/(1r) 5/(1r)2 5/(1r)3

5/(1r)4 100/(1r)4 - r 5

- Excel rate (4, 5, -100, 100) or Goalseek

- Quoted Bond yield (annualized) 10

- Effective annual rate 1.052 -1 .1025 or 10.25

11

Bond Chart Example

- Issuer coupon maturity ask

price ask yield - US Govt 6.00 Oct 08 99.0625 3.33

- Problems 5 6

current price ()

coupon rate is 6 of 100 face 3 paid every 6

months

current YTM ()

final coupon and 100 face paid then

12

Term Structure of Interest RatesInterest Rate

Forecasting

- . . . Problem 4 (equivalent)

- Assume the 2 year rate is 1 higher than the 1

year rate and you have a two year horizon. - You have 2 strategies

- 1. Put a 1000 into a bond with a 2 yr. maturity

- 2. Put a 1000 into a 1 year bond, which you will

roll over at the end of one year?

13

Key Learning Points

- Term structure of interest rates

- Expectations hypothesis and forward rates

- Real and nominal interest rates

- Inflation

- Real and nominal cash flows

- Bond yields

- Yields are inversely related to bond prices

- Long maturity bonds are most sensitive to changes

in yields

Recommended