Sample new presentation for Chicago Equity Partners

1 / 29

Title:

Sample new presentation for Chicago Equity Partners

Description:

... Tech sector trading at twice P/E multiple of any other growth sector, ... Today, Tech sector trades at a similar multiple, of around 30, with other growth ... – PowerPoint PPT presentation

Number of Views:69

Avg rating:3.0/5.0

Title: Sample new presentation for Chicago Equity Partners

1

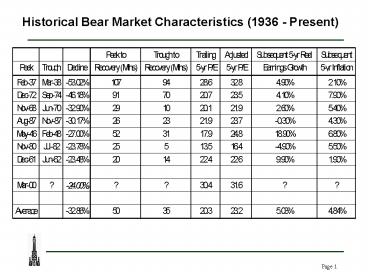

Historical Bear Market Characteristics (1936 -

Present)

2

Peak-to-Recovery Time

vs.

Decline Severity (1936-Present)

100

80

60

2

R

0.8638

40

20

0

-20

-60.00

-50.00

-40.00

-30.00

-20.00

-10.00

0.00

Market Decline

3

Accessor Growth FundJuly 17, 2001Presented

byChicago Equity Partners

Michael P. Wagner Director Client Service

David C. Coughenour, CFA Managing

Director Research

4

Facts About Chicago Equity Partners

Assets Under Management March 31, 2001 7.2

Billion Clients Assets (M)

No. Corporate 2,524.3 35 Foundations

Endowments 1,008.5 31 Funds 2,258.6

4 High Net Worth 169.4 17 Public

1,021.1 12 Taft-Hartley 194.6 8

Total 7,176.5 107

Products Assets (M) Large Cap Equity

5,167.4 Mid Cap Equity 648.2 Small Cap

Equity 305.4 Customized Balanced

Accounts 986.2 Fixed Income

69.3 Total 7,176.5

People Portfolio Managers/Trading 16 Client

Service/Sales/Marketing 15

Compliance/Operations/Technology 6

Administrative 6 Total 43

5

Investment Philosophy

- Balance investment returns against client

benchmark with explicit risk parameters - Remain sector neutral

- Maintain fully invested portfolios

- Employ proprietary quantitative methods to

analyze fundamental information and identify

value in efficient markets

6

Strategy

- Goal is to add incremental value (alpha) over

benchmark by being - Disciplined

- Objective

- Consistent

Performance results are gross of fees.

7

Stock Selection

Stock Universe

- Sort by Industries

11 proprietary model factors

- Momentum factors

- Estimate momentum

- Earnings surprise

- Downward earnings revision

- Upward earnings revision

- Earnings Change

- Value factors

- P/E ratio

- Price/book ratio

- Cash flow

- Dividend discount model

- Quality factors

- Forecasted earnings dispersion

- Leverage

Model Output

Stock Ranking by alpha

8

Stock Ranking within Industry by Forecasted Return

Highest

Buy

30

30

Sell

Lowest

9

- Market has been dominated by sharply higher

volatility and violent factor rotation over the

past six months.

Accessor Growth fund 105 stocks

CEP inception w/Accessor fund 70 stocks

10

Active Risk

- If an investment manager is being compared to a

performance benchmark, then the difference in

return between his portfolio return and the

benchmarks return is of crucial importance, the

difference is active return. - The Active Risk is defined as the standard

deviation of the active return. Active Risk is

also known as Tracking Error, since it

describes how well the portfolio can track the

benchmark.

11

Portfolio Construction/Risk Control

- Goal Make sure we get consistent returns for

the risk we take - Understand Benchmark Characteristics

- Set Tracking Error Constraint

- Target Excess Return

- Build Portfolios

12

Portfolio Construction

Eliminate

Neutralize

Capitalization Variance

Emphasize

Stock Selection

13

Sector Weightings

As of 5/31/01

14

Accessor Growth Fund

as of 05/31/01

15

Example-American Home Products (AHP)

16

Why Not Sector/Size/Style Bets?

- Over a long time frame a diversified portfolio

substantially outperforms the various sector

components on a risk-adjusted basis. - The long-term winning sectors in terms of return

are nearly impossible to identify--even after the

fact! - On a short-term basis, there is substantial

evidence against the efficacy of market timing --

whether this is measured in size and style terms,

or in sector terms.

17

Source Ibbotson Associates

18

Source PSN

19

Source PSN

20

Large Cap Core Universe (1995-99)

Excess Annualized Return

vs.

Annualized Tracking Error

Percentage Outperforming lt 3 Tracking Error

57 gt 3 Tracking Error 31

10

Average -2.0

5

0

Annualized Excess Return ()

-5

-10

-15

0

1

2

3

4

5

6

7

8

9

10

Source PSN

Annualized Tracking Error ()

21

Why a Risk-Controlled Approach?

- Empirical evidence supports the contention that

active management can consistently add value over

3-5 years, if it is pursued in a risk-controlled

fashion. - Broad evidence of negative value-added stems from

analysis of broad segments, rather than focusing

on specific sub-segments of investment approach

or tracking error. - Most managers detract value because of the

excessive impact of market timing elements that

are negative on average, overwhelming the impact

of positive average security selection. - Higher tracking error approaches can beat the

benchmark by a larger amount, but have a higher

probability of underperforming and by a greater

amount. This is because efficiency is lost as

tracking error increases. The trade-off between

return and tracking error is not uniform, largely

due to the constraint of a long-only portfolio.

22

- Value-based rally began as typical earnings-based

factors drove a sector-oriented rally - This was followed by a focus on P/E, Downward

Revisions and Earnings Dispersion across sectors - This has been followed by an emphasis on

non-earnings value metrics like Dividend Yield

and P/B

23

Our Factor Approach

- Our model represents a balance of estimate

momentum, quality and value factors. This

weighting is determined based upon the long-term

average preferences of the market. - In the growth universe, the value metrics keep us

out of the tails and drive us toward the center

of the distribution. However, the primary

drivers of the growth stocks over the past decade

have been earnings growth related factors. - Value factors as primary drivers of relative

growth stock performance, which we have seen over

the past six months, are anomalous and signal

broader market and economic uncertainty, which is

likely to be temporary.

24

Our Factor Approach

- Our models factor weights will adjust

dynamically if there is a persistent trend

movement in the markets preferences for

particular factors in the way that it values

securities. This moderated approach prevents

getting burned by factor shifts and subsequent

reversals. - If sharp factor rotation continues we dont want

to chase the market by shifting weightings to

factors that the market has most recently

favored.

25

- Historical market averages are above long-term

average P/E of 14 (measured from 1926-present) - Current SP 500 trading at both trailing and

forward P/E of 21 - Before bubble burst, SP Tech sector trading at

twice P/E multiple of any other growth sector,

like Healthcare or Consumer Staples - Today, Tech sector trades at a similar multiple,

of around 30, with other growth sectors - Value sectors trading in high teens to low-mid 20

multiples, which are high relative to historical

standards - All sectors high relative to historical ranges,

though we dont see any disconnect between

sectors that we saw previously.

26

- Market is probably telling us that this is a

cyclical downturn - Above -average earnings growth path should return

to an above average earnings growth path with the

catalyst being an underlying improvement in

economic structural productivity

27

- Model incorporates upward and downward revisions

in analyst estimates for earnings in the current

and next fiscal years. - Model also incorporates the magnitude of the

change in estimates over the last one and three

months. - We dont use long-term growth rates, which are

always highly inflated, our research shows this

factor has no reliable bearing on stock price

movements. - We dont use price targets and we dont forecast

multiples. - We compare one stock versus another, given

current multiples and the analyst consensus

earnings expectations. - We use information that is relevant in

forecasting near and intermediate-term stock

moves-are the earnings expectations moving up or

down and by how much.

28

SP/BARRA Growth - SP/BARRA Value Performance

History

Growth Outperformed Value

Value Outperformed Growth

Source Ibbotson Associates

29

Footnotes

Information on Accessor Funds, Inc. may not be

distributed to the public unless it is preceded

or accompanied by the prospectuses of Accessor

Funds, Inc. which describe in detail the

investment policies, management fees, and other

matters of interest to the prospective investor.

Through separate prospectuses, the Fund offers

two classes of shares, the Investor Class Shares

and the Advisor Class Shares, shown here. Each

class has different expenses that would affect

performance. Alloset is proprietary asset

allocation software of Accessor Capital

Management LP. Please contact Accessor Funds at

800-759-3504 for a free copy of the current

prospectus. PLEASE READ THE PROSPECTUSES

CAREFULLY BEFORE YOU INVEST OR SEND MONEY. The

performance data quoted represents past

performance of the Advisor Class shares and is

not indicative of future results. The investment

return and principal value of an investment will

fluctuate so that an investors shares, when

redeemed, may be worth more or less than their

original cost. The benchmark comparative

indices represent unmanaged returns on various

financial assets and does not reflect fees or

expenses. You cannot invest in an index. Past

performance is not a predictor of future results.

Except as otherwise indicated, the information

set forth herein has been extracted from various

public and private sources. Accessor makes no

representations as to the accuracy of the

information, nor has Accessor attempted

independently to verify it. All trademarks are

the property of their respective organizations.

The prospectuses of Accessor Funds, Inc.

describe in detail the Funds investment

policies, all fees and expenses and other matters

of interest to the prospective investor. Alloset

is the proprietary asset allocation software of

Accessor Capital Management LP. Alloset and

Accessor are registered trademarks of Accessor

Capital Management. 1. a. Effective March 16,

2000, Chicago Equity Partners Corp. manages the

Growth Fund (formerly managed by State Street

Bank and Trust Company from inception to July 20,

1997 and Geewax Terker and Company from July 21,

1997 to March 15, 2000). 2. The SP 500 Index is

an unmanaged index of 500 common stocks chosen to

reflect the industries in the U.S. economy. The

SP 500/BARRA Growth Index is an unmanaged index

of growth stocks in the SP 500 Index. Large

capitalization growth stocks are the stocks

within the SP 500 that generally have high

expected earnings growth and higher than average

price-to-book ratios. The SP 500/BARRA Value

Index is an unmanaged index of value stocks in

the SP 500. Large capitalization value stocks

are the stocks within the SP 500 that generally

are priced below the market average based on

earnings and lower than average price-to-book

ratios. The indices represent unmanaged returns

on various financial assets. Investments cannot

be made directly in an index. Past performance is

not a predictor of future results. Except as

otherwise indicated, the information set forth

herein has been extracted from various public and

private sources. Accessor makes no

representations as to the accuracy of the

information, nor has Accessor attempted to

independently verify it. All trademarks are the

property if their respective organizations.

Recommended

CrystalGraphics Presentations