Two Types of Investments: - PowerPoint PPT Presentation

1 / 39

Title:

Two Types of Investments:

Description:

Equity-indexed CDs base yield on change in a stock market index. 7. Money Market Mutual Funds ... Can be exchanged for specified number of common stock shares ... – PowerPoint PPT presentation

Number of Views:132

Avg rating:3.0/5.0

Title: Two Types of Investments:

1

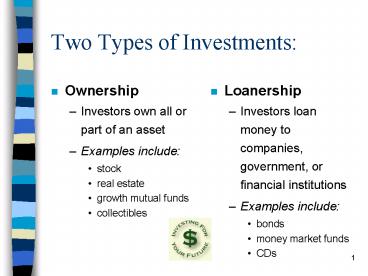

Two Types of Investments

- Ownership

- Investors own all or part of an asset

- Examples include

- stock

- real estate

- growth mutual funds

- collectibles

- Loanership

- Investors loan money to companies, government, or

financial institutions - Examples include

- bonds

- money market funds

- CDs

2

Characteristics of Fixed-Income Investments

- Interest can be fixed or change with market rates

- Subject to interest rate risk

- Many have a fixed maturity date

- Principal generally returned at maturity

3

Why Buy Fixed Income Investments?

- Adds diversification to portfolio

- Lower volatility than stock

- Predictability of investment return

- Some offer tax advantages

- Capital gains potential

4

Categories of Fixed-Income Investments

- Securities sold at banks

- Various types of bonds

- Other fixed-income investments sold by brokers

5

Certificates of Deposit (CDs)

- Sometimes called time deposits

- Pay fixed rate of interest for fixed time period

- Typical maturities 30 days to 5 years

- Higher return (generally) on longer maturities

- Bank CDs are federally insured

6

CDs

- Penalty charged for early withdrawals

- CDs sold by brokers as well as banks

- Broker-sold CDs often pay higher yields

- Equity-indexed CDs base yield on change in a

stock market index

7

Money Market Mutual Funds

- Fund portfolio consisting of high-quality,

short-term debt instruments - Professionally-managed

- Securities mature in 90 days or less

- Minimum initial deposit varies

- Purchase through investment companies or

financial advisors

8

MMMFs

- Different from bank money market deposit accounts

(MMDAs) - No FDIC insurance

- Limited check-writing

- Can select tax-exempt MMMFs invest in short term

government securities

9

U.S. Savings Bonds

- Lowest-denomination federal debt

- Income exempt from state/local tax

- Federal tax can be deferred for up to 30 years or

until bond is cashed in - Must be held six months to redeem

- 3-month interest penalty bonds not held five

years

10

U.S. Savings Bonds

- EE bonds sold at half of face value

- Interest rate 90 of 5-year Treasuries

- I bonds sold at full face value

- Pay fixed rate inflation adjustment

- Automatic purchase with EasySaver

- Earnings may be tax-free (education)

11

Bonds An Overview

- Debts of corporations or governments

- Promise specified interest rate (coupon) and

return of principal at maturity - Typically sold by brokers

- Subject to interest rate risk

12

More About Bonds

- Interest rate fluctuations affect long-term bonds

more than short-term bonds - Some bonds subject to call risk (issuer retires

bonds and reissues at lower rate) - Par (face) value is typically 1,000 (5,000 for

municipal bonds)

13

Bond Ratings

- Ratings predict ability of a bond issuer to repay

debt - Investment grade top 4 grades

- Baa to Aaa from Moodys

- BBB to AAA from Standard Poors

- Lower ratings substandard grade (a.k.a., junk,

high yield)

14

U.S.Treasury Securities

- Considered the safest fixed-income investment

- Sold at periodic auctions

- Earnings exempt from state and local tax

(principal of reciprocal immunity) - 1,000 minimum with 1,000 increments

15

U.S. Treasuries

- Types of Treasury Securities

- Bills 3-, and 6-month maturities

- Notes 2-, 5-, and 10-year maturities

- Bonds No longer available

- Can purchase through Treasury Direct at

www.publicdebt.treas.gov - Interest is credited electronically

16

Municipal Bonds

- Debt of state/local governments or government

entities - Generally sold in 5,000 increments

- Two types

- General Obligation (GO) Bond

- Revenue Bond

17

Municipal Bonds

- Interest is exempt from federal income tax

- Also state/city tax exemption- if issued by

state/city of residence - Attractive to taxpayers in 28 tax bracket and

above - Interest is paid semi-annually

18

Corporate Bonds

- Bonds issued by for-profit companies to raise

capital - Generally sold in 1,000 increments

- Interest paid semi-annually

- Generally pay higher interest than government

bonds with same maturity and credit rating

19

Corporate Bonds

- Types of corporate bonds

- Mortgage Bond backed by a companys land and

buildings - Equipment Bond backed by company equipment

(e.g., airplanes) - Debenture backed only by a companys future

earnings (most risk)

20

Convertible Bonds

- Hybrid investment which has

- Upside potential of stock

- Downside protection of bonds

- Can be exchanged for specified number of common

stock shares - As stock price increases, bond value increases

21

Convertible Bonds

- Trade-off converts to fewer shares of stock than

you can buy for bond price - Almost all convertible bonds are callable

- Available in 1,000 increments

- Can buy through convertible bond funds

22

Zero-Coupon Bonds

- Pay no (zero) periodic interest

- Sold at a deep discount

- Eventually grows to face value

- Very volatile as interest rates change (if sold

prior to maturity)

23

Zero-Coupon Bonds

- Advantages

- Low up-front cost

- Predictable return

- Disadvantage

- Annual increase in value is taxable

- Can put zeros in an IRA or buy tax-exempt zeros

to avoid this problem

24

Unit Investment Trusts

- Professionally selected portfolio of similar

securities - Packaged and sold by brokerage firms

- No ongoing portfolio management

- Sold in 1,000 units

25

UITs

- Investors promised periodic interest and return

of principal at maturity - Interest is taxable (except muni UITs)

- Advantage

- diversification and steady cash flow

- Disadvantages

- high upfront cost

- loss potential if sold prior to maturity

26

Bond Mutual Funds

- Primary objective current income

- Corporate, municipal, and Treasury bond funds

available - Advantages diversification, liquidity,

professional management, affordability - Disadvantage no fixed maturity date

27

Bond Mutual Funds

- Share price always subject to interest rate risk

- NAV decreases when interest rates rise

- Key selection criteria

- Historical performance

- Expense ratio (cost as of fund assets)

- Low cost option bond index fund

28

Mortgage-Backed Securities

- Investments in mortgage portfolios

- Principal and interest passed through

- Ginnie Maes

- 25,000 initially, 5,000 increments

- Can also buy through UITs mutual funds

- Full faith credit guarantee

- Pay slightly more than Treasury bonds

29

Mortgage Securities

- Other issuers (NOT government insured)

- Freddie Mac

- Fannie Mae

- Characteristics of mortgage securities

- uncertain maturity

- irregular monthly payments

- payments include a return of principal

30

Collateralized Mortgage Obligations (CMOs)

- Another mortgage-backed security

- Sold in 1,000 increments

- Mortgage portfolio divided into tranches with

varying maturity dates - Longer-term tranches generally pay a higher

return

31

CMOs

- Each tranche gets its principal back when

tranches before it are repaid - Characteristics

- complexity

- unpredictable repayment of principal

- payments include a return of principal

32

Fixed Annuities

- Contract with life insurance company

- Insurance company provides regular income

- Investor deposits lump sum or makes periodic

payments - Investment earnings grow tax-deferred until

withdrawal

33

Fixed Annuities

- Like a bank CD, only tax-deferred

- Guarantees a fixed rate of return for a fixed

time period - Generally 5,000 minimum investment

- Look for

- low expenses

- highly-rated insurance company

34

Preferred Stock

- Technically a form of stock, but behaves like a

bond - Preferred stock owners paid before common stock

owners if company liquidates - Typically pays fixed dividend rate

35

Preferred Stock

- Share prices vary inversely with interest rates

- Par value usually around 25 per share

- Round lot (100 shares) costs around 2,500

- Shares sold through brokerage firms

36

Guaranteed Investment Contracts (GICs)

- Fixed-income contracts issued by insurance

companies - Pay fixed interest rate for specific time period

- Commonly offered as an investment option in

401(k) plans - Sometimes called stable value funds

- Always check rating of issuer

37

Five Tips for Fixed-Income Investors

- 1. Know the risks

- 2. Beware of guarantees

- 3. Ladder your portfolio

- 4. Use zero-coupon bonds to hedge stock

investments - 5. Match investments with goals

38

Action Steps

- Reduce expenses to find money to invest

- Calculate percentage of portfolio in fixed-income

investments - Investigate fixed-income investments available in

employer savings plans - Identify fixed-income investments that match

goals and cash flow

39

Action Steps

- Compare at least three specific products

- Determine if tax-exempt investments are

appropriate for your tax bracket - Get started today!

Recommended

CrystalGraphics Presentations