Characteristics%20of%20working%20of%20SHGs - PowerPoint PPT Presentation

Title:

Characteristics%20of%20working%20of%20SHGs

Description:

Characteristics of working of SHGs The groups generate a common fund where each member contribute his/her savings on a regular basis The groups meet periodically to ... – PowerPoint PPT presentation

Number of Views:166

Avg rating:3.0/5.0

Title: Characteristics%20of%20working%20of%20SHGs

1

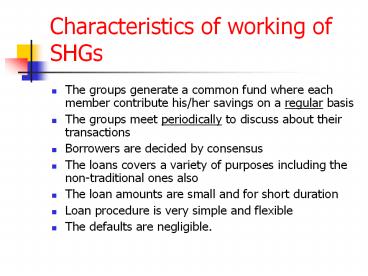

Characteristics of working of SHGs

- The groups generate a common fund where each

member contribute his/her savings on a regular

basis - The groups meet periodically to discuss about

their transactions - Borrowers are decided by consensus

- The loans covers a variety of purposes including

the non-traditional ones also - The loan amounts are small and for short duration

- Loan procedure is very simple and flexible

- The defaults are negligible.

2

Direct Linkage

Savings

Savings

Bank

Member

SHG

Credit

Credit

3

Indirect Linkage

Savings

Savings

Bank

Member

SHG

Credit

Credit

SHPI

4

Linking SHGs with Banks Advantage for Rural Poor

- Access to banks both for credit and savings

- Money is available in time and for all purposes

- Significant reduction in transaction cost of

borrowing - Loan is available without any tangible collateral

- Procedure is very simple and flexible

5

Linking SHGs with Banks Advantage for Banks

- Reduction in transaction cost of lending

- Some part of transaction cost transferred to

group (loan appraisal, follow up, and recovery) - Access to clients

- Recovery of loan

- Increased turnover with a higher margin

6

Features of Linkage Scheme

- Savings first, credit second

- No credit without savings

- Group pressure as a substitute for collateral

- Interest rate and other terms and conditions for

loan are to be decided by the group, and not by

the bank - Initially small loan, however, increased amount

over time based on good repayment record.

7

Assessment of SHGs by Banks

- Should SHGs be assessed by banks? If yes than

how? - - Banks are doing business with the groups

- - Groups should be treated as potential clients

- - Groups are informal

- - No physical collateral in loan transaction

- - Loan involves joint rather than individual

liability - - Purpose of loan is also not known to banks

- Principles of sound credit proposal like rate of

return, cost benefit ratio, or repayment capacity

can not be applied

8

Assessment of SHGs by Banks

- Norms of the group

- - Meeting (periodicity and time)

- - Savings (periodicity and amount)

- - Credit (borrower prioritization and terms)

- - Fines (system to deal with default)

- - Leadership (selection)

- Ensure that

- - The norms have been designed with consensus

- - All the members are satisfied with the norms

9

Assessment of SHGs by Banks

- Functioning of the group

- 1. Meeting

- - Whether the group is regular in conducting its

meeting or not? - 2. Member participation

- - Per cent attendance of the members in each of

the meeting - 3. Savings

- - Whether the members are regular in making

their savings contribution or not?

10

Assessment of SHGs by Banks

- 4. Credit transactions

- - Ensure that group should be involved in

lending its own fund among the members - - Recovery rate from members to group?

- 5. Fine system

- - How the group deal with the members who

default with respect to - - Making their savings contribution

- - Repaying the loan to group

- - Remain absent in the meetings

11

Assessment of SHGs by Banks

- 6. Leadership

- - How the leaders are chosen?

- - What is the tenure of leadership?

- - whether the same members are in a particular

position over time? - - Ensure the democratic functioning of the group

- 7. Maintenance of books and records

- - Activities of the group should be transparent

to each and every member - - minutes books of the meeting

- - savings and loan register

12

Assessment of SHGs by Banks

- 8. Dependence on external agent

- - Whether the group can take decisions

independently? - - Whether the loan should be made directly to

the group or through SHPI?

Recommended

CrystalGraphics Presentations

![[%20The%20Rise%20of%20Christianity%20] PowerPoint PPT Presentation](https://s3.amazonaws.com/images.powershow.com/8146520.th0.jpg?_=20190711084)