Ch 9: Strategic Control and Corporate Governance - PowerPoint PPT Presentation

1 / 43

Title:

Ch 9: Strategic Control and Corporate Governance

Description:

Informational Control. Traditional control system. strategies are formulated and top management sets goals. strategies are implemented. performance is measured ... – PowerPoint PPT presentation

Number of Views:187

Avg rating:3.0/5.0

Title: Ch 9: Strategic Control and Corporate Governance

1

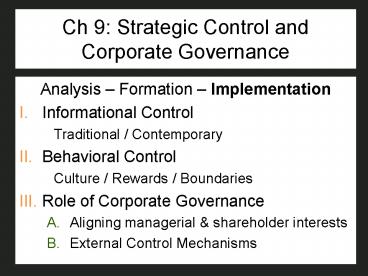

Ch 9 Strategic Control and Corporate Governance

- Analysis Formation Implementation

- Informational Control

- Traditional / Contemporary

- Behavioral Control

- Culture / Rewards / Boundaries

- Role of Corporate Governance

- Aligning managerial shareholder interests

- External Control Mechanisms

2

Strategic Control

- Strategic control -- the process of monitoring

and correcting a firms strategy and performance - Informational control

- Behavioral control

9-2

3

Informational Control

- Traditional control system

- strategies are formulated and top management sets

goals - strategies are implemented

- performance is measured against the predetermined

goal set

9-3

4

Traditional Approach to Strategic Control

- Process typically involves lengthy time lags,

often tied to the annual planning cycle - This single-loop learning control system simply

compares actual performance to a predetermined

goal

9-4

5

Traditional Approach to Strategic Control

- Most appropriate when

- Environment is stable and relatively simple

- Goals and objectives can be measured with

certainty - Little need for complex measures of performance

9-5

6

Contemporary Approach to Strategic Control

- Contemporary control system

- Continually monitoring the environments (internal

and external) - Identifying trends and events that signal the

need to revise strategies, goals and objectives - Double-loop learning

9-6

7

Contemporary Approach to Strategic Control

9-7

8

Contemporary Approach to Strategic Control

- Informational control

- the ability to respond effectively to

environmental change - Are we doing the right things?

- Outcomes

- Behavioral control

- the appropriate balance and alignment among a

firms culture, rewards, and boundaries - Are we doing things right in the implementation

of our strategy/ strategies? - Process

9-8

9

I. Informational Control

- Deals with internal environment and external

strategic context - Key question

- Do the organizations goals and strategies still

fit within the context of the current strategic

environment?

9-9

10

Informational Control

- Two key issues

- Scan and monitor external environment (general

and industry) - Continuously monitor the internal environment

9-10

11

Informational Control - Outcomes

- Common measures and controls

- Sales

- Revenue, Increased revenue

- Profit

- Customer service

- Low Cost / Differentiation / Focus

- Cost

- Quality

- Uniqueness

12

Evaluating Firm Performance (Ch 3)

- Financial ratio analysis

- Balance sheet

- Income statement

- Historical comparison

- Comparison with industry norms

- Comparison with key competitors

- Stakeholder perspective

- Employees

- Customers

- Owners

13

Financial Ratio Analysis (Ch 3)

- Five types of financial ratios

- Short-term solvency or liquidity

- Long-term solvency measures

- Asset management (or turnover)

- Profitability

- Market value

- Balanced Scorecard, Triple bottom line

14

II. Behavioral Control

- Behavioral control is focused on

implementationdoing things right - Three key control levers

- Culture

- Rewards

- Boundaries

9-14

15

Reasons for an increased emphasis on culture and

rewards

- The competitive environment is increasingly

complex and unpredictable, demanding both

flexibility and quick response to its challenges. - The implicit long-term contract between the

organization and its key employees has been

eroded.

9-15

16

Building a Strong and Effective Culture

- Organizational culture

- a system of shared values and beliefs that shape

a companys people, organizational structures,

and control systems to produce behavioral norms. - Culture acts as a means of reducing monitoring

costs

9-16

17

Building a Strong and Effective Culture

- Culture sets implicit boundaries (unwritten

standards of acceptable behavior) - Dress

- Ethical matters

- The way an organization conducts its business

- How you interact with customers, suppliers

9-17

18

Sustaining an Effective Culture

- Effective culture must be

- Cultivated

- Encouraged

- Fertilized

- Maintaining an effective culture

- Storytelling

- Rallies or pep talks by top executives

- Layout / location

9-18

19

Motivating with Rewards and Incentives

- Rewards and incentive systems

- Powerful means of influencing an organizations

culture - Focuses efforts on high-priority tasks

- Motivates individual and collective task

performance - Can be an effective motivator and control

mechanism

9-19

20

Motivating with Rewards and Incentives

- Potential downside

- Subcultures may arise in different business units

with multiple reward systems - May reflect differences among functional areas,

products, services and divisions - Individual rationality does not guarantee

organizational rationality

9-20

21

Characteristics of Effective Reward

andEvaluation Systems

9-21

22

Setting Boundaries and Constraints

- Focus efforts on strategic priorities

- Providing short-term objectives and action plans

- Specific and measurable

- Specific time horizon for attainment

- Achievable, but challenging

- Improve operational efficiency and effectiveness

- Minimizing improper and unethical conduct

9-22

23

Question

- Effective boundaries and constraints

- Tend to inhibit efficiency and effectiveness

- Distract employees who are trying to focus on

organizational priorities - Minimize improper and unethical conduct

- Tend to limit organizational growth

9-23

24

Setting Boundaries and Constraints

- Rule-based controls are most appropriate in

organizations with the following characteristics - Environments are stable and predictable.

- Employees are largely unskilled and

interchangeable. - Consistency in product and service is critical.

- The risk of malfeasance is extremely high

9-24

25

Organizational Control Alternative Approaches

9-25

26

Organizational Control Alternative Approaches

Culture

9-26

27

Organizational Control Alternative Approaches

Rules

28

Organizational Control Alternative Approaches

Rewards

29

Evolving from Boundaries (Rules)to Rewards and

Culture

- System of rewards and incentives coupled with a

strong culture - Hire the right people

- Training plays a key role

- Managerial role models are vital

- Reward systems clearly aligned with

organizational goals and objectives

9-29

30

A Note on Efficiency

- Think whole System Efficiency

- Not just piece/part efficiency

31

III. Role of Corporate Governance

- Corporation

- A mechanism created to allow different parties to

contribute capital, expertise, and labor for the

maximum benefit of each party. - Corporate governance

- the relationship among various participants in

determining the direction and performance of

corporations. - primary participants are the shareholders, the

management, and the board of directors.

9-31

32

Agency Theory

- Deals with the relationship between

- Principals who are owners of the firm

(stockholders), and the - Agents who are the people paid by principals to

perform a job on their behalf (management)

9-32

33

Agency Theory Two Problems

- The conflicting goals of principals and agents,

along with the difficulty of principals to

monitor the agents, and

- The different attitudes and preferences towards

risk of principals and agents.

9-33

34

Governance Mechanisms

- Board of directors

- a group that has a fiduciary duty to ensure that

the company is run consistently with the

long-term interests of the owners, or

shareholders, of a corporation and that acts as

an intermediary between the shareholders and

management.

9-34

35

Duties of the Board

- 1. Select, regularly evaluate, and, if necessary,

replace the CEO. Determine management

compensation. Review succession planning. - 2. Review and, where appropriate, approve the

financial objectives, major strategies, and plans

of the corporation. - 3. Provide advice and counsel to top management.

- 4. Select / recommend (to shareholders for

election) an appropriate slate of candidates for

the BOD evaluate board processes / performance. - 5. Review the adequacy of the systems to comply

with all applicable laws/regulations.

36

The New Rules for Directors

9-36

37

Governance Mechanisms

- Shareholder activism

- actions by large shareholders, both institutions

and individuals, to protect their interests when

they feel that managerial actions diverge from

shareholder value maximization.

9-37

38

TIAA-CREFs Principles on the Role of Stock in

Executive Compensation

9-38

39

External Governance Control Mechanisms

- External governance control mechanisms

- methods that ensure that managerial actions lead

to shareholder value maximization and do not harm

other stakeholder groups and that are outside the

control of the corporate governance system.

9-39

40

External Governance Control Mechanisms

- Market for corporate control

- Stock value

- Auditors

- Banks and analysts

- Regulatory bodies

- governments

- Media and public activists

9-40

41

Sarbanes-Oxley Act

- Auditors

- Barred from certain types of non-audit work

- Not allowed to destroy records for five years

- Lead partners auditing a firm should be changed

at least every five years

9-41

42

Sarbanes-Oxley Act

- CEOs and CFOs

- Must fully reveal off-balance sheet finances

- Vouch for the accuracy of information revealed

- Executives

- Must promptly reveal the sale of shares in firms

they manage - Are not allowed to sell shares when other

employees cannot

9-42

43

International

- Different rules

- Legal issues

- Different governance structures

- Ownership structures/rules

Recommended

CrystalGraphics Presentations