Measuring Default Risk from Market Price - PowerPoint PPT Presentation

1 / 8

Title:

Measuring Default Risk from Market Price

Description:

Assume that the bond has only one payment of $100 in T periods: P. Default: f*100 ... The deference induced by the fact that a large part of the credit spread ... – PowerPoint PPT presentation

Number of Views:23

Avg rating:3.0/5.0

Title: Measuring Default Risk from Market Price

1

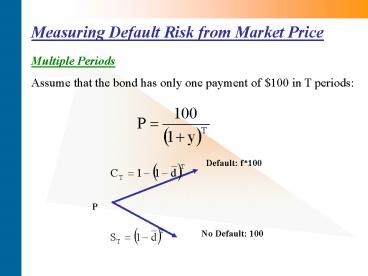

Measuring Default Risk from Market Price

Multiple Periods Assume that the bond has only

one payment of 100 in T periods

2

Measuring Default Risk from Market Price

Multiple Periods

Multiplying by (-1) and adding 1

3

Measuring Default Risk from Market Price

Which can be rewritten as

CDRT is the Cumulative Default Rate at year T.

4

Measuring Default Risk from Market Price

Assuming that the yield also reflects risk

premium

5

Measuring Default Risk from Market Price

Numerical Example IBM 10-year zero coupon bond is

rated A. The bond is traded at 7 YTM and

Treasury 10-year zero coupon bond traded at 6

YTM. The recovery rate is 45. What is the

cumulative default rate for 10 years? What is the

average marginal default rate? The Cumulative

Default Rate (CDR) for 10 years is

6

Measuring Default Risk from Market Price

7

Measuring Default Risk from Market Price

According to SP data the 10-year CDR for A rated

bond is only 3.5. The deference induced by the

fact that a large part of the credit spread

reflects a risk premium. For instance, assume

that 0.7 out of the credit spread reflects a

risk premium. In this case the 10-year CDR is

8

Measuring Default Risk from Equity Prices

The credit spread approach is only useful when

there is a good bond market data. In practice,

there are many countries that do not have a

developed bond market. In addition, the firm may

do not have publicly traded bond. In this case we

can use the firms stock price in order to

estimate the credit risk parameters