SEMINAR ON BONDS - PowerPoint PPT Presentation

1 / 75

Title:

SEMINAR ON BONDS

Description:

Most Euro zone government bonds have annual coupons and Actual/Actual year fraction ... capital gain (for bonds trading in discount) or capital loss (for bonds trading ... – PowerPoint PPT presentation

Number of Views:121

Avg rating:3.0/5.0

Title: SEMINAR ON BONDS

1

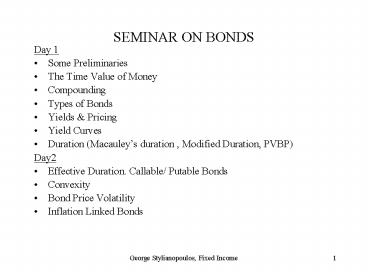

SEMINAR ON BONDS

- Day 1

- Some Preliminaries

- The Time Value of Money

- Compounding

- Types of Bonds

- Yields Pricing

- Yield Curves

- Duration (Macauleys duration , Modified

Duration, PVBP) - Day2

- Effective Duration. Callable/ Putable Bonds

- Convexity

- Bond Price Volatility

- Inflation Linked Bonds

2

Present Value and Future Value(One Interest

period)

- For securities with remaining maturity lt 1 year

(one cash flow) - PV present value ( i.e. the cash amount we pay

to buy the security) - FV future value ( i.e. the redemption amount

of the security including coupon payment, if any) - Days no of days from purchase to maturity

- Base 360, or 365, or actual, depending on the

market convention - Y yield annualized.

3

Present Value and Future Value(continued)

- Example Investing 100 now (PV) for one year at

a yield of 10 we get on maturity 110 (FV)

assuming 365 days and 365 base - Investing though, today 90 (PV) for one year

and getting on maturity 100 ,(FV) we realize a

yield of ? - 11.11

4

Present Value and Future ValueMultiple interest

periods

- The effect of compounding

- Example We invest 100 on a 3 years security

paying an annual coupon 3 once a year each year.

What will be the future value of our 100

investment? - This is because each coupon payment we assume we

reinvest at the initial yield. - The same security paying a semiannual coupon

yields us a future value of

5

Interest Calculations

- Periodic vs. Continuous compounding

- Periodic Compounding

- FVFuture Value (Principleinterest)

- PVPresent Value (Principle)

- minterest frequency per year

- nyears

- Continuous compounding the limit of periodic

compounding with m - i.e.

- e2.71828

6

Interest Calculations (continued)

- Converting periodic to continuously compounding

interest rate - Let R1 continuously compounded interest rate

- R2 periodic compounded interest rate

7

Interest Calculations (examples)

8

Definitions and Concepts

- BOND a financial obligation for which the issuer

promises to pay the bondholder a specified stream

of future cash flows, including periodic interest

payments (coupons) and a principal repayment.

Default or Credit Risk

BONDHOLDER RISK

Market (interest rates risk)

Liquidity Risk

9

Why buy bonds?

- Investors have traditionally held bonds in their

portfolios for three reasons - Income. Most bonds provide their holders with

fixed income. On a set schedule, annually or

semiannually or quarterly the issuer sends the

bondholder a fixed payment - Diversification. Although diversification does

not ensure against loss, an investor can

diversify a portfolio across different asset

classes that perform independently in market

cycles to reduce the risk of low, or even

negative, returns. - Protection against Economic Slowdown or

Deflation.

10

Types of Bonds

- Bonds are differentiated according to the issuer,

and according to the type of their cash flows. - The major bond markets are

- 1) sovereign bonds (issued by governments)

- 2) corporate bonds (issued by corporates)

- There are many types of bonds, depending on their

cash flows among which are - Fixed rate bonds (bonds paying periodically fixed

coupon) - Floating rate notes (bonds that their coupons are

linked to an index, e.g Libor) - Callables I.e. bonds giving the right to the

issuer to buy them back before their maturity

(e.g. mortgages) - Bonds with Sinking Funds for example a 7 10

years corporate bond, paying down 10 of the

principal amount annually beginning in year 3 - Zero Coupon bonds bonds that are just redeemed

on maturity without any other periodic payment of

interest

11

Market conventions

- Bonds are quoted in the secondary market as a

percentage of their face value (Clean or Flat

Price) without including the accruals (if any). - Example

- Market quote for Hell Rep 3.10 due 20 April 10

on 7th Oct 2005 with settlement 12th Oct 2005

was - 101.12 - 101.14 This means that to buy Face

value 1 million Euro of this bond we have to pay

1,011,400 Euro 175 days (days from 20 April

2005 to 12 Oct 2005) accrued interest

(3.101751,000,000/365) 14863.01 Euro total

1,026,263.01 Euro - Dirty or Full Price of the Bond Clean Price

Accruals. - Coupon frequency (annual or semiannual), and the

days count convention (e.g. 30/360, Act/360,

Act/Act, etc..) is predetermined by the issuer. - Most Euro zone government bonds have annual

coupons and Actual/Actual year fraction - US Treasuries, Italian BTPs, U.K. Gilts have

semiannual coupons and Actual/Actual year

fractions.

12

Yields

- The main types of yields are the following

- Current Yield

- Yc current yield

- c annual coupon payment

- P Clean price

- Simple Yield to maturity (or Japanese Yield)

- Yssimple yield to maturity

- Rredemption value (most cases 100)

- PClean Price

- Tsmdays from settlement to maturity

- cannual coupon

- Yield to maturity is the value of the discount

rate in the bond equation that equates the

present value of all future cash payments of the

bond to the current market price

13

Yield to Maturity. The Bond Equation

- B dirty price of the bond Present Value of the

bonds cash flows discounted by the yield to

maturity - Ci cash flow of the bond at time ti with 1ltiltn

- Yyield to maturity

- Analytically. Having a bond paying an annual

coupon c for n years and redeems at par (100),

yielding to maturity y its present value is

given by

14

Yield to Maturity. The Bond Equation (continued)

- For any coupon frequency the present value of the

bond ( i.e. its dirty price is given by the

formula - B dirty pricePV

- R redemption value (usually 100)

- Y Yield to maturity

- m coupon frequency

- DSC days from settlement to next coupon payment

- E no of days between coupon dates

15

Yields (continued)

- Example

- Bond Hell Rep. 3.10 due on 20th April 10. Market

price 101.14 as at 7th Oct 2005, settlement 12th

Oct 2005. Calculate its current yield, simple

yield and yield to maturity.

16

Current Yield, Simple Yield, Yield to Maturity

Examples

17

Bloomberg Yield Analysis screen for GGB 3.60

JUL 16

18

Current vs. Japanese and Yield to Maturity

- Current yield is the quickest check of the yield

of a bond but not reliable as it ignores any

change in the value of the capital invested.

Investors today do not rely on current yield. - Simple Yield to Maturity although more accurate

than current yield is still not the ideal measure

of yield because 1)it assumes constant capital

gain (for bonds trading in discount) or capital

loss (for bonds trading at premium), and 2) it

ignores the time value of money. It is simple. - Yield to Maturity is the most accurate measure of

a bonds yield as it explicitly recognizes the

importance of points in time at which different

cash payments from a bond are to be received.

Implicit in the definition of the yield to

maturity is the assumption that the investor will

be able to reinvest all coupon payments at at a

rate equal to yield to maturity at which he

bought his bond. This risk is known as the

reinvestment risk.

19

ZERO COUPON BONDS

- Zero coupon bonds are bonds that pay no coupons,

or bonds of which their coupons have been striped - Cash flows wise are the simplest fixed rate bonds

as they have a single cash flow on maturity. The

bond equation is simplified as there are no

coupon payments to - BBond price (dirtyclean)

- Rredemption value (usually 100)

- Y yield to maturity

- DSM days from settlement to maturity

- E base of the year (360,365)

20

ZERO COUPON BONDS (examples)

21

The PriceYield Function

22

Yield Curves

- A yield curve plots the yields to maturity of a

series of bonds of the same quality ( i.e. same

credit) against their respective terms to

maturity. - A yield curve can exhibit the following 4 shapes

- Normal or positively sloped yield curve A curve

in which short-term interest rates are lower than

longer term interest rates - Inverted yield curve or negatively sloped A

curve in which long -term interest rates are

lower than that of shorter term interest rates. - Flat yield curve Short-term and long term

interest rates are roughly equal. - Humped yield curve A humped yield curve is

positively sloped from the short maturity sector

to the intermediate sector, but negatively sloped

from the intermediate to the long sector.

23

Normal Yield Curve

24

Inverted Yield Curve

25

Flat Yield Curve

26

Humped Yield Curve

27

Theories explaining the yield curve shape

- Liquidity preference theory. This theory states

that that the yield curve will be upward sloping

because of the preference of investors for

liquidity. Liquidity here is defined as the

ability to recover the principal of the bond in a

reasonably short period of time. - Market segmentation theory. This theory views

the fixed income market as a series of distinct

markets, segregated by maturity. Individual

investors and issuers are restricted to specific

maturity sectors. Thus investors and issuers do

not have complete maturity flexibility. - Expectations theory. According to the

expectations theory the shape of the yield curve

reflects the market consensus forecast of future

interest rate levels.

28

Summing up theories of the yield curve shape

- Yield curves tend to exhibit a modestly positive

slope over long periods of time, reflecting the

market participants desire for liquidity.

Liquidity preference - Market segmentation shows up as an influence on

yield curve shape, particularly over short term

horizons (e.g. auction periods) and within

specific issuer sectors. Imbalances of supply

and demand create bumps on the yield curve at

various maturity points for specific periods of

time. - Finally there are an adequate number of investors

with maturity flexibility (e.g. mutual funds) to

validate a degree of expectations reflected in

the yield curve shape. Inflation fears tend to

steepen the slope of the yield curve while

disinflation expectations act to flatten or

invert the yield curve.

29

The higher credit quality, the flatter the yield

curve

30

Germany (AAA)- Belgium (AA) Greece (A)

31

Determinants of the absolute level of the yield

curve

- A nominal interest rate can be dissected into

three basic components. - Nominal interest rate real interest rate

inflation premium risk premium - The real interest rate is the compensation to

the investor for deferring consumption to a

future period. Even if inflation is stable at 0

a risk less investment (e.g US Treasury) must

offer a positive rate of return. - The inflation premium is intended to preserve the

purchasing power of the investor over time. This

premium reflects an expectation of the future

inflation level over the lifespan of the

investment. - The risk premium protects the investor against

all other potential negatives, including a)

credit or default risk, b) call or early

redemption risk, c) liquidity or marketability

risk, d) risk of unexpected changes in inflation

(i.e. the degree of unpredictability in assessing

future inflation.

32

DURATION

- The weighted average maturity of a bonds

cashflows, where the present values of the cash

flows serve as weights - the term to maturity of the equivalent zero

coupon bond - the balancing point of a bonds cash flow stream,

where the cash flows are expressed in terms of

present value

Cash flows

Time in years

0

Duration

33

Calculation of duration of a 10 year bond with

coupon 4 priced at par to yield 4 on maturity

34

Factors influencing Duration

- Term to maturity

- Coupon rate

- Accrued interest

- Market yield level

- Sinking fund features

- Call provisions

- Passage of time

35

The influence of each factor on duration

36

Factors influencing duration- A rule of thumb

- As a rule of thumb

- Long Maturity, Low Coupon, Low Yield High

Duration

37

Duration of 7 coupon bonds of various

maturitiesEach bond is priced at par YTM 7

38

The durationterm to maturity relationship for

coupon bearing bonds

39

The durationterm to maturity relationship for

zero coupon bonds

40

The durations of 15 year Govt. Bonds for several

coupon rates. Yield environment 7

41

The durationcoupon rate relationship

42

The Durationaccrued interest relationship

A bonds duration is inversely related to the

amount of accrued interest attached to the bond.

Hellenic Republic due 20/5/13, 7.50 price 111,

settlement 19/5/99, YTM6.29, Duration

8.80 price 111, settlement 20/5/99, YTM6.29,

Duration9.39

43

The Durationmarket yield relationship

44

The duration-market yield relationship

45

Calculation of the duration of a 7 coupon,

10-year corporate bond with a sinking fund paying

down10of the principal amount annually,

beginning in year 3. The bond is priced at par to

yield 7 to maturity

46

The relative contributions to the price of a 7

coupon, 10year corporate bond with (1) no sinking

fund provisions and (2) a 70 sinker. Each bond

is priced at par to yield 7 to maturity.

Sinking fund provisions lower the duration of a

bond by reducing the average maturity of the

principal repayment.

47

The durationpassage of time relationship

- As time passes a bonds duration falls at an

increasing rate. The duration decline is a

natural consequence of the progressively smaller

set of remaining coupon cash flows and the

approaching principal repayment.

48

Modified Duration

- Macaulays duration can be used as a measure of a

bonds risk. A longer duration implies a higher

degree of price sensitivity and therefore,

greater market risk. - Macaulays duration in order to be more accurate

as a measure of bond risk requires a

modification. This revised version of duration is

called modified duration and is calculated as

follows - MDmodified duration

- Dduration

- Yyield to maturity

49

Modified Duration (..continued)

- Modified duration calculates the percentage

change in a bond price for one basis point change

in yield. - Bdirty price of the bond

- Yyield to maturity

50

Price Value of a Basis Point (PVBP,or PV01)

- Price Value of a Basis point is a measure that

shows how much the price of the bond (or a

portfolio) will change for a shift of 1 b.p. in

yield . It is simply the Modified Duration times

the dirty price of the bond - PV01 is widely used as it shows with good

approximation how much money a bond or a

portfolio of bonds will profit (loose) from a

favorable (adverse) shifts in yield(s).

51

Mathematics of Duration

- Bdirty price of the bond

- ci cash flow of the bond at time ti, 1lt i lt n

- yyield to maturity

- D Duration, MD Modified Duration

52

continued Mathematics of Duration

- Bdirty price of the bond,

- MDModified Duration,

- PV01Present Value of a basis point.

53

Duration, Modified Duration, PV01 (example)

54

Effective Duration

- Effective Duration is

- For an option-free bond the bonds modified

duration - A measure of the average maturity of a bonds

cash flows. For a callable bond the average

maturity of the cash flows is shortened by the

possibility of early redemption of the issue. - A sophisticated weighted average of the modified

durations that a callable (putable) bond can

have. - A simple weighted average of the modified

duration of the option-free component and the

modified duration of the option component - For a callable (putable) bond effective duration

lies between the modified duration to call (put)

and the modified duration to maturity. It

approaches the MD to call(put) as yields

fall(rise), and the MD to maturity as yields

rise(fall).

55

Callable Bonds

- A callable bond is a bond that gives the right to

the issuer to buy it back at a pre-specified

price over a predetermined period - The price of a callable bond is calculated as the

price of a an equivalent non callable bond of

similar structure less the value of the call

option(s) attached - The call option value is subtracted because the

bondholder implicitly sells the call to the

issuer of the bond.

Noncallable Bond Price

Call Option Value

Callable Bond Price

-

- The crossover price is the price at which the

Yield to Call and the yield to Maturity are

equal. The yield level is termed crossover yield

56

The price yield curves for a callable bond and

for two non callable counterparts a non callable

maturing on the first call date and the a non

callable maturing on the final maturity date

MMMaturity Date Bond C1C1Call Date

Bond C2C2Callable Bond

M

Crossover Yield, Crossover Price

C1

Bond price

C2

C1

M

C2

Market Yield ()

57

Assessing the Duration of a Callable Bond

- There are 3 ways of assessing a callable bond

duration - Calculate the duration to call (DTC) and duration

to maturity (DTM). Use DTC if the bonds market

price exceeds the crossover price, and use DTM if

the bonds market price exceeds the crossover

price - Calculate a weighted average duration based on a

subjective assessment of the probability of call.

- Calculate an effective, or option- adjusted

duration by using an option valuation model.

58

Factors influencing a callable bonds duration

- Selecting either DTC or DTM

- Market price gt Crossover price Modified DTC

- Market priceltCrossover price

Modified DTM

Under this (more naive) approach the factors

influencing duration are the market price and the

bonds crossover price

59

Factors influencing duration of a callable bond

- B. The weighted average duration approach

- The modified DTC and the modified DTM that form

the lower and upper boundaries respectively of

the bonds modified duration. - The current yield environment. A low yield

environment increases the probability of future

calls. - The expected trend in interest rates. A trend to

lower rates increases the probability of early

redemption - The expected variability in interest rates. The

greater the variability the more probable it is

that the bond will be redeemed early.

DTC

DTM

AVGDUR

60

Factors influencing the duration of a callable

bond

- C. Effective duration approach

- Call date(s). An early call date reduces a

bonds effective duration. - Maturity date. A short remaining term to

maturity lowers a bonds effective duration. - Call (i.e. strike) price. A low call price

shortens effective duration. - Market price. A high market price (i.e. low

yield) decreases duration. - Market yield volatility. A high degree of yield

volatility reduces duration.

61

Example of Calculating either DTC or DTM

A 10 year 6 corporate bond NC5 at 103.00 with a

market price at 106.00. At market price 106.00

the modified duration of a non callable bond

maturing in 10 years is 7.48 At the same price

(106.00) the modified duration of a non callable

bond with maturity 5 years and redeeming at

103.00 is 4.26

Yield Environment Price to Maturity Price to Call

5.21 106.00 105.71

5.30 105.32 105.32

6 100.00 102.24

Crossover price and Yield

Market price (106.00) gt than crossover price

(105.32) therefore the duration of the callable

bond is 4.26

62

Example of calculating the weighted average

duration

A 10 year 6 corporate bond NC5 at 103.00 with a

market price at 106.00

Pc probability of call DTC 4.26 DTM 7.48

Yield Environment Bond Price Probability of Call

2 135.93 1

3 125.59 0.9

4 116.22 0.8

5 107.72 0.7

5.21 106.00 0.600

6 100.00 0.4

7 92.98 0.3

8 86.58 0.2

9 80.75 0.1

10 75.42 0

AVGDUR4.26X0.607.48X0.405.55

63

Example of calculating the effective duration

A 10 year 6 corporate bond NC5 at 103.00 with a

market price at 106.00

Effective Duration(modified duration of a

noncallable X Wb)( modified duration of the call

option X Wc) Wb the market value weight of the

bond component (expressed in decimal form) Wc

1-Wb the market value weight of the call option

(expressed in decimal form) Wb Wc 1 A non-

callable bond with same maturity of the callable

trades at 110.00 yielding 4.72 and having a

modified duration of 7.56 The value of the call

option is Callable bond price noncallable bond

price call option value 106 110 call option

value, therefore call option value - 4 An

option is extremely price sensitive and therefore

has a large duration. If the call option has a

modified duration of 50 then Effective duration

of the callable bond 7.56X110/10650X(-4/106)7.5

6X1.037736-50X1.88679 5.96

64

Putable Bonds

- A putable bond is a bond that gives the right to

the holder to sell it back at a pre-specified

price on a predetermined put date. - The price of a putable bond is calculated as the

price of a an equivalent non putable bond of

similar structure plus the value of the put

option attached - The put option value is added because the

bondholder implicitly buys the put option from

the issuer of the bond.

Putable Bond Price Option-free bond price put

option value

- A putable bond is attractive because the holder

(not the issuer) has the discretion to exercise

the put option. - In a bull market it behaves like an option free

bond, (with significant price gains) whilst in a

bear market downside price losses are limited.

65

Comparison of callable and putable bonds

Feature Callable Putable

Option definition A call option gives its holder the right to buy the bond at a pre-specified price on a pre-specified date. A put option gives its holder the right to sell a bond at a pre-specified price at a pre-specified date.

Option holder Issuer Investor

Market availability Widespread Limited Supply

Option Strike Price Typically at a premium Typically at par

Option Exercise A series of call dates and call prices A single put date

In the money when Market price gt call price Market price lt put price

Out the money when Market price lt call price Market gt put price

Yield vs. an option-free bond Higher yield Lower yield

66

The Limitations of Modified Duration

- Instantaneous yield change. Although it is

possible to experience sizable intraday, yield

shifts in turbulent financial markets, yield

shifts typically occur over time. - Small change in yield. Modified duration is a

better approximation of the price behavior of the

bond for small yield changes (10 bps or less) - Parallel shifts in yield. It would be a rarity

to find all bond yields moving in tandem.

Short-term bond yields fluctuate more than

long-term bond yields. Nonparallel yield shifts

often occur.

67

The Limitations of Modified Duration (example)

68

CONVEXITY

Positive Convexity Region

69

Definitions of Convexity

- Convexity is the second derivative of the

priceyield function and it shows the rate of

change of modified duration as yields shift - Convexity can be defined as the difference

between the actual bond price and the bond price

predicted by the modified duration line. - The term convexity arises from the fact that

priceyield curve is convex to the origin of the

graph. This curvature creates the convexity

effect - Convexity enhances a bonds price performance in

both bull and bear markets but not in a uniform

manner. - The larger the changes in yield the greater the

convexity effect. - A decline in yields creates stronger convexity

impacts than does an equivalent rise in yields.

70

Convexity and the PriceYield function

- The nonlinear priceyield function can be

analyzed as a Taylor series of derivatives

71

Factors influencing Convexity

- Duration. Convexity is positively related to the

duration of the underlying bond. It is also an

increasing function of duration - Cash flow distribution. Convexity is positively

related to the degree of dispersion in a bonds

cash flows. - Market yield volatility. High Volatility in

interest rates creates large convexity effects. - Direction of yield change. Convexity is more

positively influenced by a downward movement in

yields than by an upward surge in yields

72

The ConvexityDuration relationship

- Price,yield curves for 3,10, 30 years bonds with

a coupon 7 and price at par to yield 7

73

Convexitycash flow distribution relationship

The priceyield curves of a 30year Bond with a

coupon 7 priced at par to yield 7 and a

duration of 13.25 and a zero coupon bond of same

duration(I.e. 13.25 years to maturity) at 7 yield

P30,30years coupon bond

P0,zero coupon bond

74

The convexityyield volatility relationship

High Volatility in interest rates creates large

convexity effects

75

The Convexitydirection of yield change

relationship

- Convexity effects are greater in declining yield

environment than in rising yield environment.

Recommended

CrystalGraphics Presentations