CGA Lesson - PowerPoint PPT Presentation

1 / 31

Title:

CGA Lesson

Description:

Is there a Provision to 'Bump' certain Assets like in the Parent/Sub ... the provision to bump is the same exactly the same because again the ITA just ... – PowerPoint PPT presentation

Number of Views:324

Avg rating:3.0/5.0

Title: CGA Lesson

1

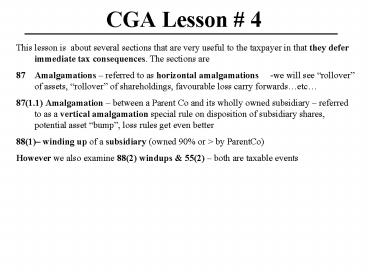

CGA Lesson 4

- This lesson is about several sections that are

very useful to the taxpayer in that they defer

immediate tax consequences. The sections are - Amalgamations referred to as horizontal

amalgamations -we will see rollover of

assets, rollover of shareholdings, favourable

loss carry forwardsetc - 87(1.1) Amalgamation between a Parent Co and

its wholly owned subsidiary referred to as a

vertical amalgamation special rule on disposition

of subsidiary shares, potential asset bump,

loss rules get even better - 88(1) winding up of a subsidiary (owned 90 or gt

by ParentCo) - However we also examine 88(2) windups 55(2)

both are taxable events

2

Horizontal Vs. Vertical Amalgamation

3

The spirit of the law is to defer or minimize

immediate tax consequences on the event but

there are many rules to accomplish this and they

address the following items -what happens to the

assets liabilities of each predecessor T2 -what

happens to the Tax Accounts of each (CDA,

RDTOH,etc..) -what happens to the shareholders

and their shares they owned -special rule on loss

continuity - there is concern for TAX PUC of the

new shares issued - there is a concern for

Gifting as well

Also in order for corporations to amalgamate they

must both be incorporated in the same

jurisdiction- but you may get a continuance.

4

Section 87(1) says an amalgamation is when two

or more Canadian corporations (predecessor corps)

merge to form a new corporation (Amalco). -all

property of the predecessors become property of

the new corp -all liabilities of the predecessors

becomes liabilities of the new corp -all

shareholders of the predecessors become s/hers of

the new corp if it is a short form vertical

amalgamation per s.87(1.1)then the shares of

the ParentCo can just be retained by the s/hers

and be deemed to be shares of the new Amalco

5

Assets Liabilities

S.87(2)(a) deems year-ends for the predecessor

corps immediately before the amalgamation date

and deems a new corp to be formed on the amalco

date (you can pick its year-end) -there are about

a dozen pages in the ITA detailing what happens

to the asset liabilities of the former

predecessor companies- But they all do the same

thing they state that the former tax costs of

the assets liabilities are flowed through or

picked up by the new Amalco. -this flowing

through provides for a rollover effect of the

assets from the predecessor to the Amalco. For

example a capital property like land (Acb

10,000) flows to the Amalco with the same cost.

Transfers do NOT happen at FMV.

6

- Assets Liabilities continued

- Additional examples

- -87(2)(d)depreciable property transfers over at

its UCC balance..and historical Capital Cost

deemed to flow through as well so as to preserve

potential recapture on a future sale - 80.01(3) inter-company debts get special mention-

they are extinguished at their cost amounts- thus

no losses - Assets are NOT deemed disposed of so you can

have CCA claims in the last year

Tax Accounts..flow through too

CDA, RDTOH, GRIP (with some exceptions), Reserves

all flow from the predecessor balances to the new

entity

As you can see it is mostly just a matter of

adding/arithmetic

7

Losses do they transfer over?

87(2.1) governs the flow through of the

predecessor losses to the Amalco the

acquisition of control rules apply -these rules

say that IF an acquisition of control has

occurred upon amalgamation then capital losses of

the predecessor corps cannot go forward to the

amalco and non-capital losses can only go forward

if a same or similar business is carried on by

the Amalco. The point to be made in 87(2.1) is

that (subject to the acquisition of control

rules) the predecessor corp losses are deductible

by the Amalco starting in its very first year .

The Amalco steps into the shoes of the

predecessors shoes for timing of when losses

occurred. So the Amalco has to be aware of the

original dates of loss to apply them correctly.

Remember amalgamation may have triggered a short

year for a predecessor corp. it still counts as

a full year in the application of losses rules.

8

Losses continued..

- -predecessor losses flow forward to the Amalco

- -- losses that flowed up from one predecessor to

the Amalco cannot be applied back to the other

predecessor corp - losses that the Amalco itself may generate from

its own business can never go back to the

predecessor corps (Except in a vertical

amalgamation (Parentco subsidiary amalgamate,

then losses of the new Amalco itself can be

applied back against the predecessor ParentCo

only) - Lesson notes examples 4-3 shows loss rules

date with a short/ stub period stresses

importance of the application of loss dates .

Before March 23/2004 7 years forward up to

Jan.2006 its 10 years.after that its 20 years

page 9

9

PUC Rule 87(3)

-it is a simple rule .the total tax puc of the

new Amalco shares is limited to the tax puc of

the two predecessor shares -however per 87(3)

there is no puc allowed for shares of one

predecessor company that were held by another

predecessor company.. so when dealing with a

Parent CO and Subsidiary amalgamation the Puc of

the subsidiary shares is eliminated and cannot be

allocated to the Amalco shares. -a puc reduction

is applied to all shares..this might be unfair

to some so to eliminate this you may elect to

issue a different class of shares to different

predecessor s/hers. 87(3.1) but apparently there

are complexities attached which make it difficult

for taxpayers to utilize

10

Predecessor Shares

General Rule s.87(4) for horizontal

amalgamationsit says that the shares of the

predecessor companies are deemed disposed of for

proceeds equal to their ACB .and the new shares

have a cost equal to that same ACBthis is in

effect a rollover of the old shares for new

shares Special Rule -however this rule changes

in a vertical amalgamation ..the shareholders of

the Parent Co follow the same rule the shares

are exchanged for their ACB. -but the shares

that the ParentCo owns of the subsidiary are

deemed to be disposed per a formula- we will look

at this in a moment

11

Gifting Concern in s.87(4)

- -if a shareholder exchanges shares old shares for

new shares having a FMV less than that of the FMV

of the old shares and it is reasonable to regard

any of the excess as an benefit amount that the

s/her desired to confer on a related

person..then proceeds of disposition will be

deemed to be - Lesser of

- -the ACB plus the gift amount OR

- Fmv of the old shares

- Plus there is no bump to the acb of the new

shares - See ex 4-5

12

Summarizing 87(1) Amalgamations

-all assets liabilities transfer over to the

new Amalco at the predecessor tax costs - thus

no immediate tax consequences -since assets are

not deemed disposed of, CCA may be claimed in the

final year of the predecessor T2s -all Tax

Accounts like CDA , CSOH , RDTOH, reserves etc

transfer over at the same values -the

amalgamation date deems year-ends for the

predecessor T2s and the Amalco is a new

entity -losses (subject to the acquisition of

control rules) go forward -predecessor shares are

deemed disposed for their acb and the new Amalco

shares have the same acb and the same tax puc as

the old -there is a provision to discourage

gifting

13

Parent Wholly Owned Subsidiary Amalgamation

87(1.1)

- the rules for deemed year-ends, cca claims

assets liabilities tax accounts transferring

over to the Amalco are all the same - We will see a new rule for the disposition of the

shares that the Parent Co owns of the Subsidiary

corp that could result in - A capital gain OR

- a

capital loss.AND if there is a loss it will be

denied BUT there could be a limited ability to

BUMP the cost base of certain assets of the

subsidiary. - -we will see an additional rule for

losses.allowing for any new Amalco generated

loss to be carried back to the Parent CO - PUC?- sub puc is eliminated ,only allowed the Puc

of the ParentCo

14

We are talking about this situation

15

Addtional Loss Rule 87(2.11)

-first lets remember the predecessor loss carry

forward rules are the same Amalco can only

apply them forward -Why is there no concern about

the subject to the acquisition of control rules

? Because before the S/hers owned the

Parent,.. Parent owns sub now s/hers own

Amalco there has been no acquisition of control

there is really no change at all -the new

rule is that now losses that are incurred or

generated by the new Amalco can be applied back

against the predecessor PARENT CO (note

Parentco only , never the subsidiary)

16

The Rule for the Deemed Disposition of the Subs

shares. Note this section refers you to 88(1)b

We seldom see gains because 99 of the time Puc

is or lt the acb

17

Disposition of the Subsidiary Shares that were

Owned by the Parent Co s.87(11)

S/hers X,Y,Z

S/hers X, Y, Z

Parent

Amalco

Sub

A special rule exists for the deemed disposition

of the sub shares

Amalgamation date

18

What if the ACB of the subsidiary shares is

really greater than the net tax cost of the

subs assets? is this not really a Loss on my

share investment? Section 87(11)(b) addresses

this issue.

19

Example 4-6

20

What does this look like? Example 4-6 continued

Amalgamate on Oct1/2007

Sept 30 year-ends

Parentco

Montfort

Sub shares cost 100,000

Amalco

Kimfort

Kimball

Subsidiary

Kimball paid a 20,000 dividend to Montfort

21

Subsidiary (Kimball) assets were before the

amalgamation

22

Example 4-6 continuednote how no loss occurs

yet the cost of the shares is gt the tax cost of

the subs assets

23

What about Possible Asset Bump? Loss carryback? .

24

Winding Up a Subsidiary Owned 90 or More S.88(1)

- -winding up normally means following the

procedures for winding up per the Corporations

Act.giving notice to dissolve and surrender its

charter..88(1) section applies automatically if

both the Parent sub are Canadian corps and the

parent owns at least 90 of the sub.and the

other s/hers (if any) deal at arms length with

the parent - in the course of the wind up

- 1) all assets liabilities of the sub transfer

to the Parent - on a tax deferred basis - 2) The Parent has a deemed disposition of the

shares of the subsidiary that it owns potential

for gain and a bump on assets- it is the exact

same rule we saw on Parent / Sub amalgamation - 3) The Subsidiaries Losses have a special

application rule

25

Asset Disposition Rules s.88(1)

-when the assets are transferred from the Sub to

the Parent they are deemed disposed of for their

COST AMOUNT (def. 248) -this effects a

rollover of the assets from sub to Parent.but

since they are deemed disposed of they are not

on hand at year-end so no CCA claims can be made

on them in the year of transfer. -if there were

s/hers other than the ParentCo the assets go out

at FMV -there is no deemed year-end of the sub

because of its announcement to commence winding

up..it commences to wind up transfers assets

over time to the Parent and when it is finished

it will determine its own year end at that

time -inter-company debt they can elect to

extinguish it at the cost amount -tax accounts

transfer over for the same values

26

Sub Winding Up into Its ParentCo

BEFORE

AFTER

ParentCo

ParentCo

Owns its own assets plus shares in sub as an

asset

Owns its subs assets liabilities

Sub

Assets Liabilities

Sub is gone, wound up

Winds up

Transfers assets up to Parentco

27

Deemed Disposition of the Subs Shares Held by the

ParentCo s.88(1)(b)

-this is the same rule as we saw for the Parent

/ Sub Amalgamation..it is exactly the same

because they refer to each others 87(11) refers

to s. 88(1)(b) for the calculation -so the

shares are deemed disposed for greater of

1) the lesser of PUC of the shares OR

cost

amount of the net assets reserves 2) acb of the

shares so no loss can occur , but a

gain could result

28

Is there a Provision to Bump certain Assets

like in the Parent/Sub amalgamation Rules YES

s. 88(1)c d

- -the provision to bump is the same exactly the

same because again the ITA just refers each

section to the other see 87(11) - -if the subsidiarys shares have an ACB that

exceeds - The total of

- The net tax cost of the assets of the sub AND

- 2) All dividends ever received by the

Parentco. - Then you can bump certain non depreciable

assets up to their FMV .BUT remember the

date for the FMV calculation is determined by

when the Parent last acquired control of the sub

if the Parent always controlled then no bump

is possible..Bump would be lost, unusable .

29

Transfer of Losses in Parent-Sub Windup

S.88(1.1) (1.2)allow the subsidiaries losses

(assuming they had some ) to flow through to the

ParentCo BUT they may only be deducted by the

ParentCo.for taxation years commencing after the

commencement of the winding up of the

subsidiary Simple example Assume both Parentco

Sub have normal year-ends of Dec.31, 2007 and in

April /07 the sub commences to wind up and

finishes winding up in Sept / 07when can the

Parentco deduct any losses of the sub? Not until

the next fiscal period 2008. Parentco Jan

1/07______________________________ Dec31/07

Sub Jan 1/07 ____________________Sept./07

fully wound up

Can deduct in

2008

30

Uses of

S.88(1)

Then Duncan Ltd is wound up into Alberni Ltd

31

Winding Up of a Canadian Corporation S.88(2)

- This is a taxable event- in fact we are looking

at two levels of taxation. The first is at the

corporate level as the corp liquidates its assets

and secondly when the available net funds are

finally distributed to the shareholder as a

windup dividend. - Normally you would expect to undergo the

following procedures - The corp liquidates its assets at FMV- this may

trigger gains recapture that it will have to

pay tax on. - The corp pays off all of its debts , including

the tax liability from 1 above. - Any cash or unsold assets are distributed to the

s/her as a wind up dividend per 84(2). Assets go

out at FMV per s.69(5).

Recommended

CrystalGraphics Presentations