Portfolio Weights - PowerPoint PPT Presentation

1 / 16

Title:

Portfolio Weights

Description:

The portfolio weights must add up to 1.00 or 100%. Portfolio Return ... (SML) is graphed as the line through the risk-free investment and the market. ... – PowerPoint PPT presentation

Number of Views:106

Avg rating:3.0/5.0

Title: Portfolio Weights

1

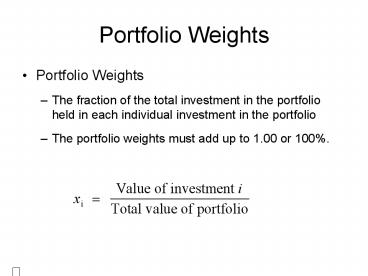

Portfolio Weights

- Portfolio Weights

- The fraction of the total investment in the

portfolio held in each individual investment in

the portfolio - The portfolio weights must add up to 1.00 or 100.

2

Portfolio Return

- Then the return on the portfolio, Rp , is the

weighted average of the returns on the

investments in the portfolio, where the weights

correspond to portfolio weights.

3

Portfolio Risk

- By combining stocks into a portfolio, we reduce

risk through diversification. - The amount of risk that is eliminated in a

portfolio depends on the degree to which the

stocks face common risks and their prices move

together. - To find the risk of a portfolio, one must know

the degree to which the stocks returns move

together.

4

Portfolio Risk Depends on

- Covariance

- The expected product of the deviations of two

returns from their means - Correlation

- A measure of the common risk shared by stocks

that does not depend on their volatility

5

Variance of a portfolio

6

The Effect of Correlation

- Correlation has no effect on the expected return

of a portfolio. However, the volatility of the

portfolio will differ depending on the

correlation. - The lower the correlation, the lower the

volatility we can obtain. As the correlation

decreases, the volatility of the portfolio falls.

- The curve showing the portfolios will bend to

the left to a greater degree as shown on the

next slide.

7

Effect on Volatility and Expected Return of

Changing the Correlation

8

Portfolio Beta

- The beta of a portfolio is the weighted average

beta of the securities in the portfolio.

9

Beta and the Required Return

10

The Security Market Line

- In equilibrium, all assets and portfolios must

have the same reward-to-risk ratio and they all

must equal the reward-to-risk ratio for the

market

11

The Security Market Line

- The security market line (SML) is the

representation of market equilibrium - The slope of the SML is the reward-to-risk ratio

(E(RM) Rf) / ?M - But since the beta for the market is ALWAYS equal

to one, the slope can be rewritten - Slope E(RM) Rf market risk premium

12

The Capital Asset Pricing Model (CAPM)

- The capital asset pricing model defines the

relationship between risk and return - E(RA) Rf ?A(E(RM) Rf)

- If we know an assets systematic risk, we can use

the CAPM to determine its expected return - This is true whether we are talking about

financial assets or physical assets

13

The Security Market Line

- There is a linear relationship between a stocks

beta and its expected return (See figure on next

slide). The security market line (SML) is graphed

as the line through the risk-free investment and

the market. - According to the CAPM, if the expected return and

beta for individual securities are plotted, they

should all fall along the SML.

14

SML

15

Estimating Beta from Historical Returns

- Beta corresponds to the slope of the best-fitting

line (Characteristic Line) in the plot of the

securitys excess returns versus the market

excess return.

16

Total vs Systematic Risk

- Consider the following information

- Standard Deviation Beta

- Security C 20 1.25

- Security K 30 0.95

- Which security has more total risk?

- Which security has more systematic risk?

- Which security should have the higher expected

return?

Recommended

CrystalGraphics Presentations