Bonds

1 / 15

Title: Bonds

1

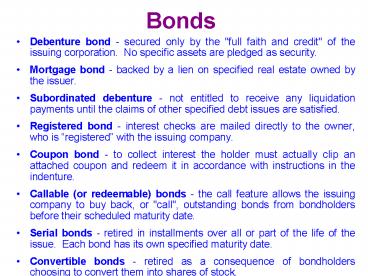

Bonds

- Debenture bond - secured only by the "full faith

and credit" of the issuing corporation. No

specific assets are pledged as security. - Mortgage bond - backed by a lien on specified

real estate owned by the issuer. - Subordinated debenture - not entitled to receive

any liquidation payments until the claims of

other specified debt issues are satisfied. - Registered bond - interest checks are mailed

directly to the owner, who is registered with

the issuing company. - Coupon bond - to collect interest the holder must

actually clip an attached coupon and redeem it in

accordance with instructions in the indenture. - Callable (or redeemable) bonds - the call feature

allows the issuing company to buy back, or

"call", outstanding bonds from bondholders before

their scheduled maturity date. - Serial bonds - retired in installments over all

or part of the life of the issue. Each bond has

its own specified maturity date. - Convertible bonds - retired as a consequence of

bondholders choosing to convert them into shares

of stock.

2

Bonds Sold at Face

- On January 1, 2000, Masterwear Industries issued

700,000 of 12 bonds. Interest of 42,000 is

payable semiannually on June 30 and December 31.

The bonds mature in three years an

unrealistically short maturity to shorten the

illustration. The entire bond issue was sold in

a private placement to United Intergroup, Inc. at

face amount. - At Issuance (January 1)

- Masterwear (Issuer)

- Cash 700,000 Bonds payable (face

amount) 700,000United (Investor)Investment

in bonds (face amount) 700,000 Cash 700,000

3

Bonds Issued Between Interest Dates

- All bonds sell at their price plus any interest

that has accrued since the last interest date. - Illustration - On March 1, 2000, Masterwear

Industries issued 700,000 of 12 bonds, dated

January 1. Interest of 42,000 is payable

semiannually on June 30 and December 31. The

bonds mature in three years. The entire bond

issue was purchased by United Intergroup, Inc.

for 700,000 plus 14,000 accrued interest. - 700,000 x 12 x 2/12 14,000 face

annual fraction of the accrued value

rate annual

period interest - At Issuance (March 1)

- Masterwear (Issuer)

- Cash (price plus accrued interest)

714,000 Bonds payable (face amount)

700,000 Interest payable (accrued

interest) 14,000 - United (Investor)Investment in bonds (face

amount) 700,000Interest

receivable (accrued interest) 14,000 Cash

(price plus accrued interest)

714,000

4

Determining the Selling Price

- A bond issue will be priced by the marketplace to

yield the market rate of interest for securities

of similar risk and maturity. - Illustration - On January 1, 2000, Masterwear

Industries issued 700,000 of 12 bonds, dated

January 1. Interest is payable semiannually on

June 30 and December 31. The bonds mature in

three years. The market yield for bonds of

similar risk and maturity is 14. The entire

bond issue was purchased by United Intergroup,

Inc. - Present value (price) of the bonds Present

Values - Interest 42,000 x 4.76654

200,195 - Principal 700,000 x 0.66634 466,438

- Present value (price) of the bonds 666,633

- present value of an ordinary annuity of 1

n6, i7 (Table 6-4) - present value of 1 n6, i7 (Table 6-2)

5

Determining Interest - Effective Interest Method

- Interest accrues on an outstanding debt at a

constant percentage of the debt each period.

Interest each period is recorded as the effective

market rate of interest multiplied by the

outstanding balance of the debt (during the

interest period). - Continuing the previous example, interest

recorded (as expense to the issuer and revenue to

the investor) for the first six-month interest

period is 46,664 - 666,633 x 14 2 46,664

- Outstanding Balance Effective Rate

Effective Interest

6

Amortization Schedule - Discount

- Effective

Increase in Outstanding - Interest

Balance Balance - 666,633

- 1 .07 (666,633) 42,000 4,664 671,297

- 2 .07 (671,297) 42,000 4,991 676,288

- 3 .07 (676,288) 42,000 5,340 681,628

- 4 .07 (681,628) 42,000 5,714 687,342

- 5 .07 (687,342) 42,000 6,114 693,456

- 6 .07 (693,456) 42,000 6,544 700,000

7

Debt Issue Costs

- With either publicly or privately sold debt, the

issuing company will incur costs in connection

with issuing bonds or notes, such as legal and

accounting fees and printing costs in addition to

registration and underwriting fees. These debt

issue costs are recorded separately and are

amortized over the term of the related debt.

8

Installment Notes

- Notes often are paid in installments, rather than

a single amount at maturity. - Each payment includes both an amount that

represents interest and an amount that represents

a reduction of principal. - 666,633 4.76654

139,857 amount (from Table

6A-4) installment of loan n6,

i7.0 payment - Effective

Decrease in

OutstandingCash Interest

Balance

Balance 7 x Outstanding Debt - 666,633

- 1 139,857 .07 (666,633) 46,664 93,193 573,440

- 2 139,857 .07 (573,440) 40,141 99,716 473,724

- 3 139,857 .07 (473,724) 33,161 106,696 367,028

- 4 139,857 .07 (367,028) 25,692 114,165 252,863

- 5 139,857 .07 (252,863) 17,700 122,157 130,706

- 6 139,857 .07 (130,706) 9,151 130,706 0

- 839,142 172,509 666,633

9

Troubled Debt Restructuring

- When changing the original terms of a debt

agreement is motivated by financial difficulties

experienced by the debtor (borrower), the new

arrangement is referred to as a troubled debt

restructuring. By definition, a troubled debt

restructuring involves some concessions on the

part of the creditor (lender). A troubled debt

restructuring may be achieved in either of two

ways - (a) The debt may be settled at the time of the

restructuring, or - (b) The debt may be continued, but with modified

terms.

10

DERIVATIVES

- Derivatives are financial instruments that

derive their values or contractually required

cash flows from some other security or index. - Derivative financial instruments have become

the key tools of risk management. - The most frequently used derivatives are

- o Financial futures

- o Forward contracts

- o Options

- o Interest rate swaps

- Derivatives can manage or hedge companies

exposures to risk, including interest rate risk,

price risk, and foreign exchange risk.

11

DERIVATIVES USED TO HEDGE RISK

- Hedging means taking a risk position that is

opposite to an actual position that is exposed to

risk. - The effectiveness of a hedge is influenced by

the closeness of the match between the item being

hedged and the financial instrument chosen as a

hedge. - A futures contract allows a firm to sell (or

buy) a financial instrument at a designated

future date, at todays price. - A forward contract is similar to a futures

contract but does not call for a daily cash

settlement for price changes in the underlying

contract. Gains and losses on forward contracts

are paid only when they are closed out. - An option gives its holder the right either to

buy or to sell an instrument, say a Treasury

bill, at a specified price and within a given

time period.

12

ACCOUNTING FOR DERIVATIVES

- All derivatives, no exceptions, are carried on

the balance sheet as either assets or liabilities

at fair value. - When the fair value changes, a gain or loss

occurs. - How we account for the gain or loss depends on

how the derivative is used. - 1. If the derivative is not designated as a

hedging instrument, or doesnt qualify as one,

the gain or loss is recognized immediately in

earnings. - 2. If the derivative is used to hedge against

exposure to risk, the gain or loss is either - recognized immediately in earnings along with

an offsetting loss or gain on the item being

hedged or - deferred in comprehensive income until it can

be recognized in earnings at the same time as

earnings are affected by a hedged transaction. - Which way depends on whether the derivative is

designated as a (a) fair value hedge, (b) cash

flow hedge, or (c) foreign currency hedge.

13

Fair Value Hedges

- A change in either prices or interest rates can

cause a change in the fair value of an asset, a

liability, or a commitment to buy or sell assets

or liabilities. - If a derivative is used to hedge against the

exposure to changes in the fair value, it can be

designated as a fair value hedge. - A gain or loss from a fair value hedge is

recognized immediately in earnings along with the

loss or gain from the item being hedged. - o When the derivative is adjusted to reflect

changes in fair value, the other side of the

entry is recognized as a gain or loss to be

included currently in earnings. - o At the same time, the loss or gain from changes

in the fair value (due to the risk being hedged)

of the item being hedged also is included

currently in earnings. - o So, to the extent the hedge is effective, the

gain or loss on the derivative will be offset by

the loss or gain on the item being hedged.

14

CASH FLOW HEDGES

- If a derivative is used to hedge against

exposure to changes in cash inflows or outflows

of an asset or liability or a forecasted

transaction, it can be designated as a cash flow

hedge. - When the derivative is adjusted to reflect

changes in fair value, the other side of the

entry is recognized as a gain or loss to be

deferred as a component of other comprehensive

income - included in earnings later, at the same

time as earnings are affected by the hedged

transaction. - Comprehensive income includes net income itself

and changes in elements of the balance sheet that

the FASB feels dont (yet) belong in net income

- o foreign currency translation adjustments

- o unrealized gains and losses on

available-for-sale securities - o minimum pension liability adjustments

- The portion of the gain or loss due to

ineffective hedging is reported in earnings

immediately.

15

FOREIGN CURRENCY HEDGES

- The possibility that foreign currency exchange

rates might change exposes many companies to

foreign currency risk. - A foreign currency hedge can be a hedge of

foreign currency exposure of - a firm commitment - treated as a fair value

hedge. - an available-for-sale security - treated as a

fair value hedge. - a forecasted transaction - treated as a cash

flow hedge. - a company's net investment in a foreign

operation - the gain or loss is reported in other

comprehensive income as part of the cumulative

translation adjustment.

Recommended

CrystalGraphics Presentations